In new research, Wei Cai, Andrea Prat, and Jiehang Yu evaluate how mergers affect employee satisfaction. They find that acquired firms report a decline in worker satisfaction, primarily revolving around “soft” benefits, such as workplace culture, management quality, and trust.

Mergers do not just reshape markets and shareholder returns. Finance scholars may ask whether they create value for investors, while antitrust economists ask whether a deal will raise prices or reduce competition. Recently, antitrust economists have also renewed their interest in how mergers impact wages and employment. But jobs are more than a paycheck. Employees also care about autonomy, fairness, culture, voice, advancement, and whether the organization still feels like the one they joined.

Economic theory has long suggested that these non-monetary dimensions may be vulnerable after a merger. Employment contracts do not encompass everything about a workplace. They specify salary, hours, and certain benefits, but they cannot fully spell out workplace culture, managerial style, career paths, or the degree of trust between workers and leadership. Those features are often sustained by implicit understandings rather than formal contracts. A merger changes who owns the firm and who makes decisions. Once that happens, old promises may no longer be honored or even recognized. Mergers reshape the workplace, and often in ways that employees experience negatively.

That is the central finding of our new research on mergers and acquisitions. Using a large sample of corporate deals matched to employee reviews on Glassdoor, we find that mergers are followed by a meaningful decline in worker satisfaction. The decline is not mainly about pay or formal benefits. It is concentrated instead in the softer parts of working life: culture, management quality, career opportunities, trust, and employees’ willingness to recommend their employer to others. The damage is especially strong in the firm being acquired.

Consider two widely discussed acquisitions. When Google bought YouTube in 2006, the target gained resources and scale while preserving much of what employees valued, such as operational independence, continuity in leadership, YouTube’s distinct identity, and the office location in San Bruno. But when Amazon acquired Whole Foods, many employees described a very different experience: a decentralized and participatory culture gave way to tighter performance monitoring, more centralized control, and a more punitive atmosphere. These stories point in opposite directions, which is why systematic evidence is needed.

To study the issue, we combine merger data from Refinitiv with employee reviews from Glassdoor. We focus on completed non-financial mergers between 2008 and 2020 and retain only deals where both the acquiring firm and the target have enough review activity, meaning at least one review each quarter of the merger, within three years of the transaction to track changes before and after it. After additional sample restrictions, our final dataset contains 361 mergers. For each firm and quarter, we measure average employee ratings using reviews written by current employees.

Glassdoor is especially useful for our question because it captures multiple dimensions of the work experience. We group compensation and work-life balance into “hard” dimensions, since they are more concrete and easier to write into contracts. We group culture, career opportunities, management, business outlook, CEO approval, and employees’ likelihood of recommending the firm into “soft” dimensions, since they are less tangible and less contractible.

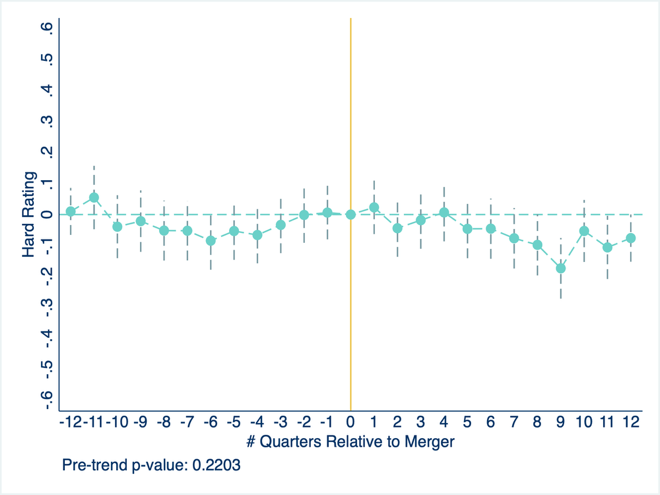

The first result is straightforward: mergers reduce employee satisfaction. After controlling for firm fixed effects, time effects, and pre-merger trends, we find that overall satisfaction falls after a merger. But the more important finding is where that decline comes from. The effect is concentrated in the soft dimensions. On average, a company’s soft ratings fall by about six percent of a standard deviation after a merger, while the hard dimensions show little movement. In other words, the typical merger does not appear to leave a large immediate mark on the more contractible parts of the job, but it does make employees feel worse about the workplace itself.

Figure 1: Change in hard (left) and soft (right) dimensions of worker satisfaction around the merger

The timing also tells an important story. The negative effects do not appear to be driven by pre-existing downward trends. In event-study estimates, satisfaction is relatively flat before the deal and then declines gradually after it, with much of the deterioration appearing a couple of quarters later and persisting afterward. That is consistent with how practitioners describe post-merger integration. The first months are often devoted to continuity. The more disruptive changes, including new systems, reporting lines, priorities, and performance metrics, arrive later.

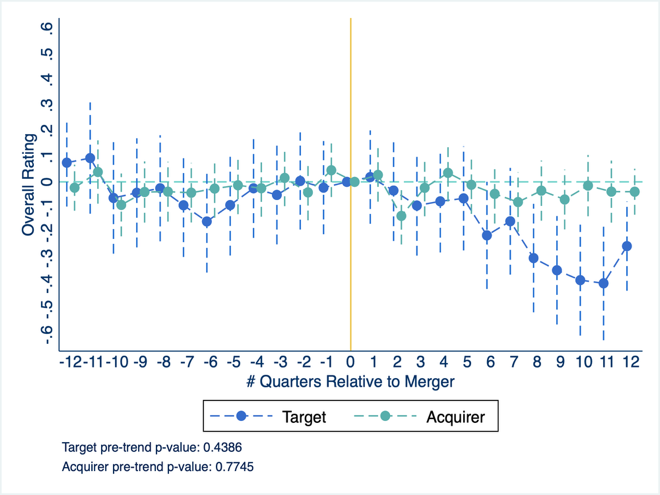

The second major result is that the losses are not evenly shared. They are much stronger in the acquired firm than in the acquiring firm. Relative to acquirers, targets see a much sharper decline in soft ratings, about 15 percent of a standard deviation more. This is exactly what incomplete-contract theories would lead us to expect. The target is the organization whose leadership changes most dramatically. It is also the place where prior relational understandings are most likely to be disrupted.

Figure 2: Change in worker satisfaction in target and acquiring firms around the merger

Why might this happen? One explanation comes from the classic idea of “breach of trust.” Workers often make firm-specific investments, such as learning internal systems, building relationships, and adapting to a company’s culture, because they believe the firm will honor implicit commitments in return, such as having a voice in the workplace, flexibility, career development, and a supportive environment. A new owner may not feel bound by those commitments. A second explanation is preference misalignment. The acquiring firm may simply want to run the business differently, with different goals, values, and tolerances, than the previous firm. Even if no promise is explicitly broken, employees may feel that the firm no longer reflects what they signed up for.

To distinguish between these mechanisms, we turn to the text of employee reviews. We use AI-generated example reviews to represent two kinds of complaints: first, that the firm has broken implicit promises to workers; second, that employees are misaligned with the new management brought in by the acquirer. We then compare those generated texts to actual Glassdoor narratives, highlighting the similarity derived from the word embedding model. Both themes become more common after mergers, especially in target firms. But when we put the mechanisms side by side, the evidence points more strongly toward breach of implicit contract as the dominant channel. Employees do not merely dislike change. They often feel that something understood, but never formally written down, has been taken away.

A natural concern is whether these results reflect who leaves or who posts reviews, rather than a real change in workplace quality. We address both issues. Because we focus on current employees, our results are not driven by laid-off workers coming back to post especially negative reviews. We also look at changes in review volume around mergers. Review activity shifts only modestly and does not display the sharp pattern that would be needed to explain the much larger and more persistent decline in ratings. Nor would a pure selection story easily explain why the negative effect is concentrated in soft rather than hard dimensions.

These findings have implications for both management and policy.

For managers, the lesson is that merger integration should not be treated as a purely operational exercise. Synergies may look attractive on a spreadsheet, but they can come with hidden organizational costs. When employees perceive that implicit commitments have been broken, morale falls. That can affect retention, effort, collaboration, and the long-run success of the deal itself. If acquirers want to preserve value, they need to pay close attention to the parts of the employment relationship that do not appear in legal contracts: trust, voice, mission, and the informal rules that make a workplace function.

For policymakers, the results suggest that the labor effects of mergers are broader than wage suppression alone. Much recent work has shown that mergers can reduce labor market competition and lower pay in concentrated markets. Our evidence adds another channel: mergers may also reduce workers’ utility through non-monetary losses. That does not mean every deal should be blocked on workplace grounds. But it does mean that evaluations of mergers should take employee welfare more seriously, especially in transactions where an acquired firm’s culture and internal organization are central to its value.

A merger can create efficiencies, new products, and new growth opportunities. But it can also dissolve the unwritten understandings that made a company a good place to work. The modern debate over mergers should recognize both sides of that ledger. Workers are not just an input into the firm. They are one of the groups most deeply changed when firms combine.

Author’s Disclosure: The authors report no conflicts of interest. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.