In new research, Xiao Dong, Paul Koh, Devesh Raval, Dominic Smith, and Brett Wendling evaluate how well divestiture remedies work for mergers in the supermarket industry. They find that past supermarket divestitures led to lower employment, reduced sales, and higher rates of exit from the market relative to comparable non-divested supermarkets.

Antitrust authorities often face a difficult choice when reviewing mergers. Blocking a transaction may prevent competitive harm, but it may also eliminate efficiencies. Challenging a merger can also impose substantial enforcement costs on regulators and pose litigation risks. Antitrust agencies therefore frequently approve mergers subject to remedies intended to address the deal’s potential risks to competition.

The most common merger remedy is divestiture. In a divestiture, the merging firms are required to sell stores, brands, or other assets to an independent buyer. The remedy succeeds only if that buyer can use the divested assets to replace the competition that would otherwise be lost because of the merger. Yet, despite the frequent use of divestiture remedies, there is limited evidence on whether they preserve competition in practice.

In a new working paper, we examine whether divestitures achieve this goal in the United States supermarket industry. Divestitures have been a common antitrust remedy in supermarket mergers because market competition primarily exists in local settings and there is significant overlap between stores. There have been more than 600 supermarkets divested in 26 mergers since 1990. Because supermarkets employ nearly three million workers and generate significant output, hitting more than $800 billion in annual sales in 2022, the success of these remedies has significant consequences for consumers, workers, and competition.

We find that store divestitures often fall short of restoring the competition lost through supermarket mergers. Divested supermarkets are substantially more likely to close, reduce employment, or lower sales after they are transferred to new owners. These outcomes appear to reflect both the quality of the stores selected for divestiture and the capabilities of the buyers that acquire them. Our paper evaluates questions about whether divestiture remedies can reliably preserve competition if authorities and judges do not carefully consider the factors that can determine success or failure.

What happens to divested stores?

We examine how divested stores fare after their divestiture using a “difference-in-differences” analysis. We compare changes in outcomes at divested stores before and after divestiture to changes at similar non-divested stores over the same period. The control group provides a plausible baseline for how the divested stores would have performed absent divestiture.

Our primary dataset is the Bureau of Labor Statistics’ Quarterly Census of Employment and Wages Longitudinal Database (QCEW LDB), which contains quarterly data on employment and payroll for U.S. establishments since 1990. We are able to match about 75% of divested stores to the QCEW LDB. We then compare divested stores to other supermarkets that are similar in age, size, chain status, and location. To avoid using stores directly affected by the divestitures as controls, we excluded stores located in the same local markets as the divested stores, as well as stores owned by the merging firms or the buyers of the divested stores.

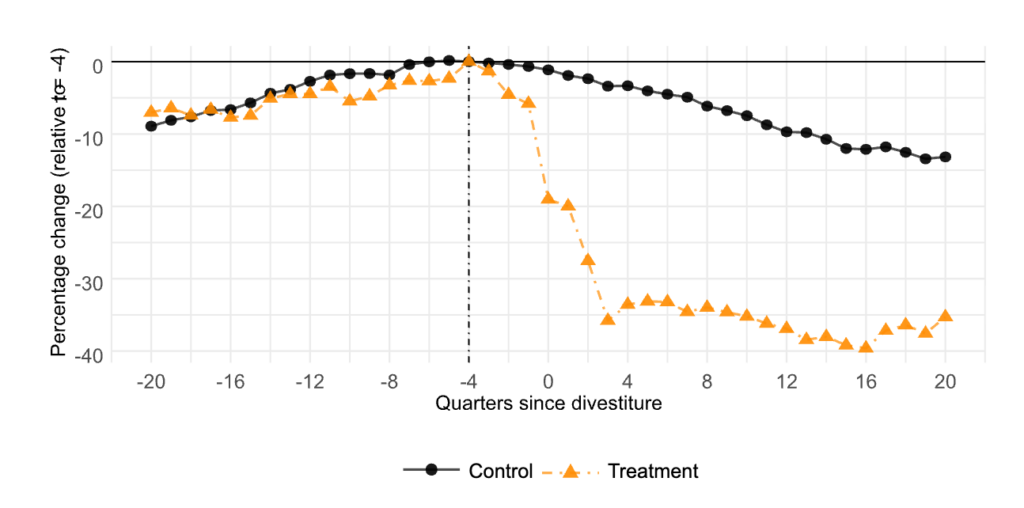

Employment at divested stores falls substantially after divestiture compared with employment at control stores. Figure 1 compares total employment at divested stores and control stores in the five years before and after divestiture, with changes measured relative to four quarters before the divestiture date. One year after divestiture, employment at divested stores declines by roughly one-third, compared with only a three percent decline at control stores. Five years after divestiture, employment at divested stores remains far below baseline, with a much larger decline than at control stores.

This decline reflects both store closures and reduced employment among surviving stores. Divested stores are 13 percentage points more likely than control stores to exit the market within one year of divestiture, and 17 percentage points more likely to exit within five years. Among stores that remain open for five years, employment falls more at divested stores than at control stores: 17 percent more after one year and 13 percent more after five years. Overall, about half of the employment decline is due to store closures.

Figure 1: Change in Total Store Employment Relative to Four Quarters Pre-Divestiture Baseline

We find additional evidence that divested stores underperform after divestiture. Average earnings of workers at divested stores fall by eight percent five years after divestiture compared with controls. In addition, in two case studies with proprietary store-level sales data, sales at divested stores fall by 20 to 30 percent relative to controls. Together, these results suggest that divested stores become weaker competitors after they are transferred to new owners.

Why do divested stores struggle?

We next examine why divested stores perform poorly. Evidence from case studies points to merging parties choosing to disproportionately divest financially weaker stores to less capable buyers. In other words, remedies depend not just on whether stores are divested, but on which stores are divested and who buys them.

We find that divested stores had lower sales and profit margins before divestiture than nearby stores retained by the merging parties. This suggests that merging firms often sold weaker assets to divestiture buyers rather than stores that were fully comparable to the ones they kept.

Buyer strength also appears to matter. Buyers of divested stores tended to operate lower-revenue stores than the merging firms before the acquisition. In one large divestiture, stores sold to buyers with relatively few stores experienced large sales declines, while stores sold to firms with larger store networks experienced sales increases. This suggests that stronger buyers may be better able to preserve the competition provided by divested stores.

Conclusion

Our results imply that past grocery divestitures were unlikely to restore the competition lost through the mergers they were intended to remedy. Divested stores contract and exit at significantly higher rates than comparable control stores, and these effects persist for several years after divestiture.

Our findings on divestitures in the supermarket industry challenge a core assumption in merger evaluation: that divestitures will generally offset the competitive risks of some mergers. We also provide evidence that divestiture outcomes depend on both the quality of the assets sold and the capabilities of the buyers that acquire them. These findings suggest that divestiture remedies may require greater scrutiny of both the assets being sold and the buyers selected to operate them.

Our study focuses on supermarkets, an industry in which successful entry and expansion require more than simply acquiring stores. Buyers may need a capable distribution network, attractive private-label products, and the right price-quality tradeoff to compete effectively. Divestiture remedies may therefore be especially difficult to implement successfully in supermarkets. Future work should examine whether our findings generalize to other industries through systematic studies of multiple divestiture events within the same industry.

Author’s Disclosure: The author reports no conflicts of interest. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.