Finbar Curtin and Matthew Burgess’ recent article analyzing the relationship between the climate and economy has been interpreted as a study proving that climate change’s impact on economic growth is weak. Garvin Jabusch argues that this interpretation is wrong. Rather, the article concludes that statistical estimates of this relationship are limited by data and future capital allocation should favor a ‘no-regrets’ approach anchored in observable cost curves and productive capacity.

Some interpreted the authors’ finding to suggest that there is no evidence that climate change affects the economy. Economist Tyler Cowen flagged it on his blog with two sentences: “Important stuff, I hope to hear more about this. The whole climate to gdp [sic] transmission thing does not seem to be working very well?” While Cowen’s reading is ambiguous about his interpretation, his readers articulated a common skepticism that climate change has little economic impact. To clarify, this is not what Curtin and Burgess argue. The first claim by some readers is about physical reality; Curtin and Burgess’s claim is about measurement. They argue that our tools are not sophisticated enough to measure the impact. The gap between these claims is where the capital-allocation question lives. The actual impact is beyond the scope of the paper.

To understand why economic models struggle, we have to look at the structural argument Curtin and Burgess make. Any model trying to predict the economic damage from climate change must make massive assumptions. These include which climate variables to use, how to weight different countries’ economies, and the choice of historical period.

Furthermore, a lot of statistical noise—random variations and big events—confuse correlations between long-term climate change and weather variation and economic growth. For example, Curtin and Burgess demonstrate that a handful of immense historical shocks—the Rwandan genocide, the collapse of the Soviet Union, the invasion of Iraq—create so much economic noise that they drive 20-50% of the statistical findings in the major studies they replicated. This is not a problem that can be fixed with more data. The limitations are baked into the methodology.

The authors are explicitly clear that their conclusion is about measurement, not mechanism. The physical reality of climate change is not in question. The existence of a negative carbon externality is not in question. What is in question is whether historical time-series data can deliver reliable, specific estimates regarding the exact magnitude of that economic damage. Their answer is that it cannot.

Currently, the published range of the estimated damage from climate change spans from near-zero at one extreme to global GDP losses of roughly 60% at the other. That massive spread does not reflect converging scientific knowledge; it reflects the fragility of the mathematical models themselves.

This matters because trillions of dollars in public and private capital are currently anchored to these exact point estimates. Central banks build scenarios based on them—those in the Network of Central Banks and Supervisors for Greening the Financial System (NGFS) use climate scenarios built on macroeconomic policy assumptions for climate stress testing. Government agencies use them to justify or dismantle policy. For example, in the United States, the Environmental Protection Agency has recently anchored its regulatory actions on estimates implying no damage at all. Both extremes of this massive, unreliable range are being treated as load-bearing foundations for decisions of civilizational scale.

Deciding under deep uncertainty

Fortunately, economics already has a framework to address how to make policy and investment decisions under “deep uncertainty.” Economists like Martin Weitzman argue that when we cannot reliably pinpoint the odds of a potentially catastrophic event, the rational response is not to sit on our hands and wait for better data. The rational response is to make decisions that perform acceptably across the entire plausible range of outcomes.

Curtin and Burgess explicitly endorse this approach. They favor “no-regrets” strategies—actions whose economic desirability does not depend on the final climate damage bill matching a specific projection. Examples include investing in energy efficiency, deploying renewables in geographies where they are already vastly cheaper than fossil fuels, and aggressively pursuing methane abatement. These are investments that are profitable now and in any future.

For investors, this is the core of portfolio construction under uncertainty. A reasonable skeptic might object here, asking if this “catastrophic-tail” framing overreaches in its advice for capital allocation. It is a fair objection—even the worst end of the damage range does not equate to civilizational collapse on the timeframes relevant to institutional investors. The case for transitioning capital, however, does not depend on the catastrophic tail; it holds well before one needs to invoke it. It rests on the much more mundane, mathematically robust claim that the right investments are no-regrets, or maximize returns while minimizing risk. Utility-scale solar undercuts new natural gas across most sun-rich geographies on unsubsidized cost. Battery storage is winning peaker-plant procurements against gas, on price alone. The investments that will compound reliably under deep uncertainty are those with a clear, undeniable economic rationale irrespective of measurable climate damages. That category now constitutes a large and rapidly growing share of the productive economy.

The illusion of safety in indexing

The same skeptic might argue that risk management means investing in a range of industries, both green and brown. Indeed, the conventional wisdom of modern asset management is that investing in a broad index diversifies your money, and diversification represents safety. In the presence of the kind of uncertainty Curtin and Burgess describe, both halves of that claim are entirely wrong. In institutional asset management, “risk” is not synonymous with “losing money.” Instead, it is defined as how much investments differ from the benchmark—typically a broad market index like the S&P 500. Active managers who deviate too far from their benchmark are penalized and labeled “risky,” regardless of the underlying fundamentals of their portfolios. To maintain a reasonable risk score, almost every actively managed equity portfolio is forced to hold most of the constituents of the benchmark.

This structural reality means that even funds explicitly marketed as “climate-aligned” end up with massive exposure to major fossil fuel producers simply to align with the index. Michael Santoro made a related argument in ProMarket, focusing on how fiduciary-duty interpretations prevent fund vehicles from cleanly expressing transition-timing views. The structural problem he identifies and the epistemic problem this article identifies are different layers of the same underlying failure.

This is risk amplification disguised as prudence. A portfolio deliberately constructed to mimic the broader market is actually making a massive, concentrated bet that climate damages will prove modest, and that global policy will remain highly accommodating to fossil fuel incumbents, and that cheaper green substitutes will suddenly fail to continue their decades-long cost declines.

The first two legs of that bet are highly speculative. The third leg is directly contradicted by current, real-world operating data.

Follow the cost curves, not the models

You do not actually need a reliable damage function, showing how the rising intensity of climate change corresponds to increasing economic damages, to reach the conclusion the damage function is supposed to deliver. The global energy transition is no longer a distant policy aspiration; it is an unfolding industrial reorganization backed by hard, observable data. The case derived from deep uncertainty and the case derived from industrial cost curves showing that green substitutes are getting cheaper converge on the exact same conclusion: anchor on what is measurable, because what is measurable already underwrites the transition.

Consider the physical reality. The International Energy Agency’s (IEA) Global Energy Review 2026, published with 2025 operating data, reported that solar power was the single largest contributor to global energy supply growth last year. This marked the first time any renewable energy source led primary energy supply growth, outpacing natural gas. Battery storage additions shattered previous records, and electric vehicles now account for approximately one in four new car sales globally. Crucially, China—the driver of roughly 95% of the net growth in global fossil demand since 2018—appears to have definitively crossed peak fossil fuel demand in the first half of 2025.

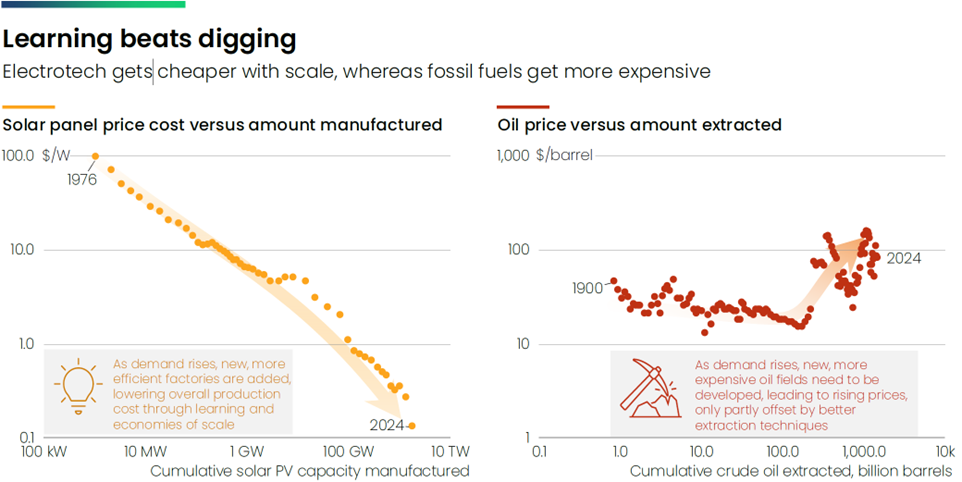

A recent report by the energy think tank Ember provides the clearest framing for why these numbers look the way they do: technologies get cheaper with scale; commodities get more expensive the deeper you dig.

Figure: Solar module prices versus cumulative manufacturing, compared with oil prices versus cumulative extraction. Source: Ember, “The Electrotech Revolution: The Shape of Things to Come,” Walter, Butler-Sloss, and Bond (September 2025). CC BY 4.0.

Since the 1980s, solar module prices have fallen 99.6% and wind installation costs have dropped 80%. Battery cell prices have plummeted 99% since 1991. Today, two-thirds of all global energy investment flows into electrotech rather than fossil fuels. Global manufacturing capacity for both solar panels and batteries already vastly exceeds the levels that the IEA calls for to achieve net-zero emissions. Even the massive infrastructure build-out required for artificial intelligence accelerates rather than slows this dynamic. While artifical intelligence is a massive emerging source of electricity demand, it is simultaneously the greatest emerging enabler of energy efficiency and grid optimization. Google’s data centers, for example, operate using roughly 84% less overhead energy per unit of compute than the typical hyperscaler across their entire fleet. A significant portion of that efficiency advantage is itself the result of AI: Google famously tasked DeepMind with applying machine learning to data center cooling, slashing cooling energy by roughly 40% immediately upon deployment. This kind of efficiency advantage compounds.

Systemic resilience and the asymmetry of the future

There is one more critical difference between the old economy and the next: how their systems fail when stressed. This architectural resilience is a form of risk protection that conventional portfolio theory misses entirely. A reasonable skeptic will rightfully point out that next-economy infrastructure faces its own climate risks. Solar farms experience destructive hail; battery storage systems can struggle in extreme heat. But the difference lies in the architecture of the systems.

A decentralized solar-plus-storage grid degrades gracefully under stress. When one node fails, the rest of the network (which can include individual homes) continues operating, and replacing the failed component is modular and cheap. By contrast, a highly centralized fossil-fired grid relies on continent-spanning fuel supply chains and massive, single-point-of-failure power plants. It does not degrade gracefully. When it fails, it fails catastrophically, and it recovers slowly. The Texas Uri event of February 2021 is a clear, recent illustration: a centralized, gas-dependent grid suffered cascading fuel-supply failures that cut power to roughly 4.5 million customers, killed at least 246 people, and took most of a week to recover. This architectural resilience is a built-in hedge against the exact kinds of deep uncertainties Curtin and Burgess formalize.

Portfolios built on this logic with decade-plus track records have demonstrated that no investor needs a reliable damage function to reach the same conclusion: the only non-self-terminating approach to capital allocation—the only one that does not undermine its own future operating conditions—is to invest in the productive capacity the Next Economy will require, rather than the systems the last economy depended on.

Ultimately, every investor holds a view on the relationship between climate change and the economy. In a world where the damage function is empirically inscrutable, the central question is not which academic estimate is exactly right. The central question is which method of portfolio construction proves robust across the entire range of possibilities.

Portfolios purposefully built around next-economy productive capacity perform acceptably if climate damages prove modest, and they perform incredibly well if damages prove severe. Conversely, portfolios heavily weighted toward legacy fossil fuels only perform well in a phenomenally narrow slice of future outcomes. That is not diversification.

The econometric damage function was always the wrong place to anchor portfolio construction. The energy transition is compounding. The damage models may not be. Capital should follow the variables that demonstrably compound.

Author comment: The author is grateful to Finbar Curtin and Matthew G. Burgess of the University of Wyoming Department of Economics for generously reviewing the characterization of their paper. All interpretive, decision-theoretic, and portfolio conclusions are the author’s alone.

Author disclosure: The author runs an investment firm whose entire framework is built on the conclusion he draws. That means readers should weigh what follows accordingly. He writes it anyway because the reading of the recent Curtin-Burgess paper that has begun to circulate from Marginal Revolution outward is, in his experience, the kind of error that calcifies into conventional wisdom if no one with a different vantage point speaks up. The vantage point the author brings is that of someone who has spent two decades allocating capital under the conditions of deep uncertainty that Curtin and Burgess have now formally described.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.