India is working on legislating new competition rules to govern artificial intelligence and other tech markets. But recommendations from a recent report by the Competition Commission of India suggest it might revert to old competition standards that will likely prove ineffectual in governing the new AI market, writes Abhineet Nayyar.

In 2024, India’s Committee on Digital Competition Law (CDCL) released a report proposing a draft Digital Competition Bill (DCB) to complement the existing antitrust regime in regulating emerging technological markets. Through its report and the draft DCB, the committee asked for an ex-ante legislative instrument to be applied to a variety of core digital services, including social networking websites, e-commerce platforms, cloud services, and online search engines. Theoretically, this ex-ante instrument would set out a list of principles to guide competition governance and deter anticompetitive behaviour in the digital economy, as opposed to utilizing ex-post rules (such as those currently found in India and the United States) that address anticompetitive behavior after they occur.

Two years on, and the draft Bill has yet to be officially introduced in Parliament, whereas digital markets have seen rapid proliferation and expansion in the meantime, most recently via the “Artificial Intelligence (AI) revolution.”

Due to their huge requirements for data, compute, and energy, large-language models (LLMs) have emerged as the ideal opportunity for deep-pocketed Big Tech firms—many of which have already invested billions in developing datasets, algorithms, and products on top of their traditional digital offerings. The financial requirements to build and scale LLMs pose the biggest challenge for startups, including Indian ones, to enter the market. Emerging market evidence indicates that Big Tech firms are also engaging in practices like the mandatory bundling of AI services, deep discounting at the model layer, or restricting cloud interoperability. Among others, these choices are likely to further entrench their dominance as the providers of AI infrastructure and restrict startups from being able to compete.

It is in this context that the Competition Commission of India (CCI) authorized a market study on “Artificial Intelligence and Competition,” the final report for which was released late last year. Prepared through a mixed-methods approach with stakeholders, the report’s aim was to study i) the current and future potential of AI technologies, ii) the scope of their use in the Indian economy, and ii) their impact on competition in the digital sphere.

Given the relative nascency of the topic, CCI’s initiative to conduct such an expansive study is laudable, but the report’s analysis of the observed market conditions and its subsequent recommendations leave much to be desired in the way of progressive antitrust action.

How is the market structured?

As the study rightfully points out, the creation of AI tools today depends on a range of inputs, including sector-specific and sector-agnostic data, compute infrastructures, and foundational and contextual models.

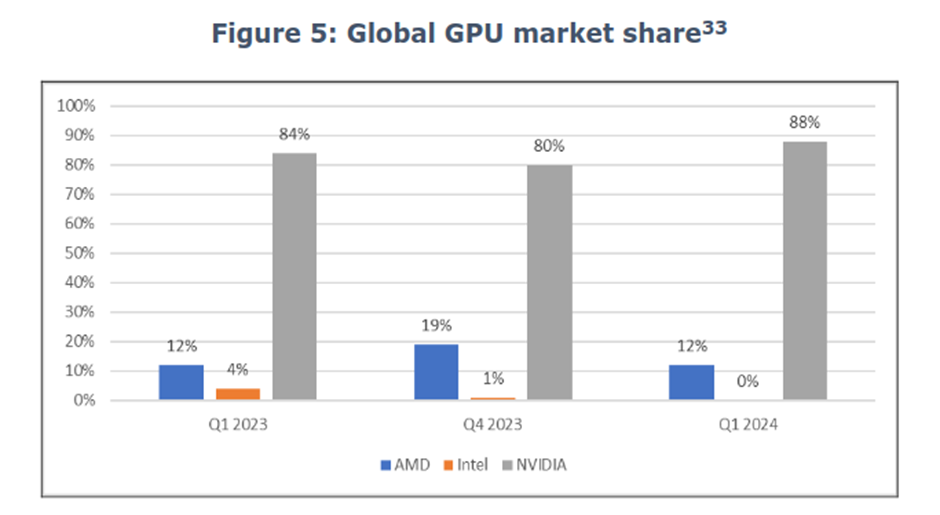

But high entry barriers for these input markets means that most, if not all, of them display clear trends of consolidation. Per the report’s own data and as shown in its “Figure 5” (reproduced below), NVIDIA holds 88% of the graphics processing unit (GPU) market share in India, a serious technical and economic bottleneck in the global AI supply chain. At another point, the report also highlights that just three firms—Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP)—control nearly 65% of the compute market, and about 46% of the data layer.

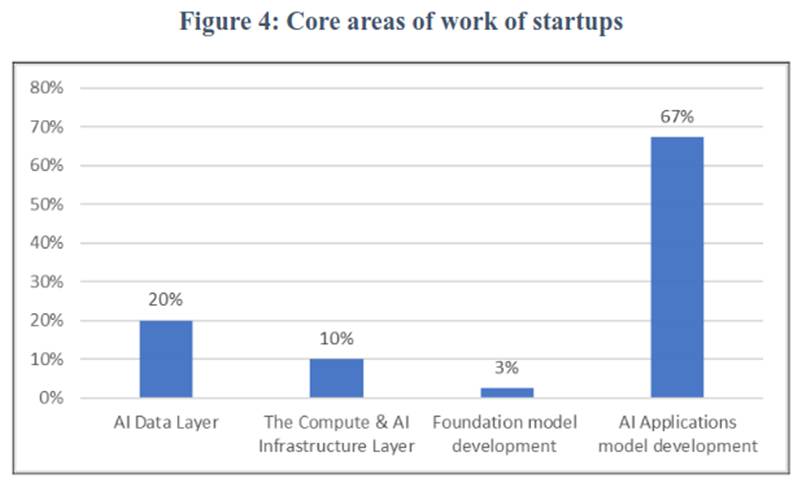

The report’s investigation into the core focus areas of Indian startups also reveals a similar insight. “Figure 4” of the report (reproduced below) shows that about two-thirds of Indian startups work in the area of developing AI applications models (i.e. the final stage before deployment), while only 3% work in foundational model development, 10% in the compute infrastructure layer, and 20% in the data layer.

For competition regulation, such centralized supply chains and their impact on local innovation priorities should be a worrying phenomenon. NVIDIA’s dominance in the infrastructure layer, for instance, has come from its strategy of bundling GPUs with its proprietary software platform—Compute Unified Device Architecture (CUDA)—which provides NVIDIA with critical network effects that raise entry barriers. Similarly, the dominance of large cloud service providers (hyperscalers) in the compute and data layers is rooted in their history as first-moving behemoths that have cornered significant shares of their respective markets.

What should be done about this consolidation?

Despite noticing clear trends of concentration in the AI economy, the study suggests an ex-post approach to competition regulation, with the goal of maximizing “consumer welfare” by allowing free competition until harm is proven, rather than predicted. Its proposals include self-auditing by AI firms, voluntary adoption of transparency measures, and focused advocacy efforts by the CCI, among others.

It is important to note here that this approach to competition law—one that simply defines consumer welfare as price-based efficiencies—has been under constant scrutiny in the case of digital markets. Experience from various countries (including India) has highlighted a few key reasons that make it difficult for an ex-post regime to respond timely and adequately in these cases.

– First, platforms mediating between two sides of a market can leverage direct and indirect network effects, providing first-movers with a clear incentive to lock in a critical amount of users, often through loss-leading tactics.

– Second, given the low scaling costs of a software solution, a successful first-mover can grow across adjacent markets with relative ease, for instance, by mandatory bundling of core services.

– And third, anticompetitive conduct by a dominant platform, say through strategic acquisitions of competitors, often looks like legal action under conventional theories of harm because of their limited focus on consumer welfare alone.

For a few years now, countries (including from the Global South) have been pushing for an ex-ante approach to competition regulation in the digital economy. By mandating dominant firms to adhere to a set of market-preserving measures, the antitrust regulator can identify and plan for harmful trends of monopolization before they set in, while also nudging private actors to serve the needs of public interest innovation in emerging areas.

Reviving ex-ante rules and the DCB

This study is CCI’s first major attempt at understanding market dynamics in the Indian AI ecosystem, and it provides a revealing insight into the ownership structures and complexities of competition in this market. Its identification of anticompetitive risks, such as high entry barriers, switching costs, self-preferencing practices, algorithmic cartelization, and price discrimination, are essential towards framing future policy proposals.

However, the report ignores troves of emerging antitrust discourse and locates its diagnosis in an antiquated understanding of market power and competition, one that prioritizes traditional metrics of consumer welfare and pricing over structural factors like technical lock-ins, bargaining power asymmetries, and data-driven consolidation. By relying on outdated theories of harm and ex-post enforcement methods, the report fails to advocate for more modern and suitable policy instruments; one very much like the draft Digital Competition Bill introduced in the beginning.

Despite its imperfections, the ex-ante DCB proposes much-needed modifications to India’s antitrust law, such as the identification of narrower markets in the digital economy and the recognition of specific anticompetitive principles. In fact, the Parliamentary Panel on the Standing Committee on Finance also recently articulated the “critical regulatory gap” left by the stalled bill. The CCI’s announcement of developing an evidence base for this law is an encouraging step, but it would be crucial to locate this exercise in a structural understanding of competition, and not one rooted in conventional standards of consumer welfare.

Author Note: I would like to thank Sadhana Sanjay and Isha Suri for their feedback in structuring and refining this article.

Author Disclosure: The author works for IT for Change, which receives funding from organizations including Both ENDS, Kotak Mahindra Bank Limited, Ford Foundation, the European Union, and the British Asian India Foundation. IT for Change’s 2025 financial statement can be found here. No funding source influenced the arguments expressed in this article or stands to benefit from them. The author reports no conflicts of interest. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.