In new research, Michele Fioretti, Aljoscha Janssen, Alessandro Iaria, Clément Mazet-Sonilhac, and Robert K. Perrons discuss how a landmark Norwegian court ruling shows how constitutional constraints on the government’s ability to retroactively change contracts can encourage private innovation and reshape entire industries.

Industries that require large, irreversible capital commitments—oil and gas, renewable energy, infrastructure—often rely on contracts with the state. Historically, contracts between private firms and a sovereign state are difficult to enforce because the state has the power to change and reverse its contractual commitments. If a firm suspects that the state might change the contractual terms once it sinks money into a project, it will hold back on further investment. Innovation goes undeveloped, technologies go unadopted, expertise sits idle, and entire industries stagnate.

This is the sovereign hold-up problem, and it is distinct from ordinary policy uncertainty. The issue is not that firms cannot predict future regulations, but that they cannot trust the state to honor existing commitments. The state, after all, can always pass a new law unless constitutional restrictions are in place.

In a new study, we provide causal evidence that sovereign hold-up risk depresses technology adoption and that constitutional constraints can mitigate it. Our setting is the North Sea oil and gas industry, where a single court ruling in 1985 transformed the investment landscape.

A court ruling that changed everything

Norway and the United Kingdom have developed the North Sea’s oil reserves side by side since the early 1970s, under strikingly similar fiscal and regulatory frameworks. Both countries allocated licenses through competitive bidding and imposed hybrid tax regimes combining royalties, corporate taxes, and sector-specific levies, with comparable investment allowances and effective tax shields. These reserves attracted the same multinational firms.

But there was a critical institutional difference. The U.K. operates under parliamentary sovereignty: Parliament cannot bind its successors, and existing contracts can be revised by ordinary legislation. Norway’s constitution, by contrast, contains Article 97—a prohibition on retroactive laws. Yet for decades, Norwegian courts applied this provision flexibly, allowing the state to impose retroactive changes to petroleum licenses in the name of public interest.

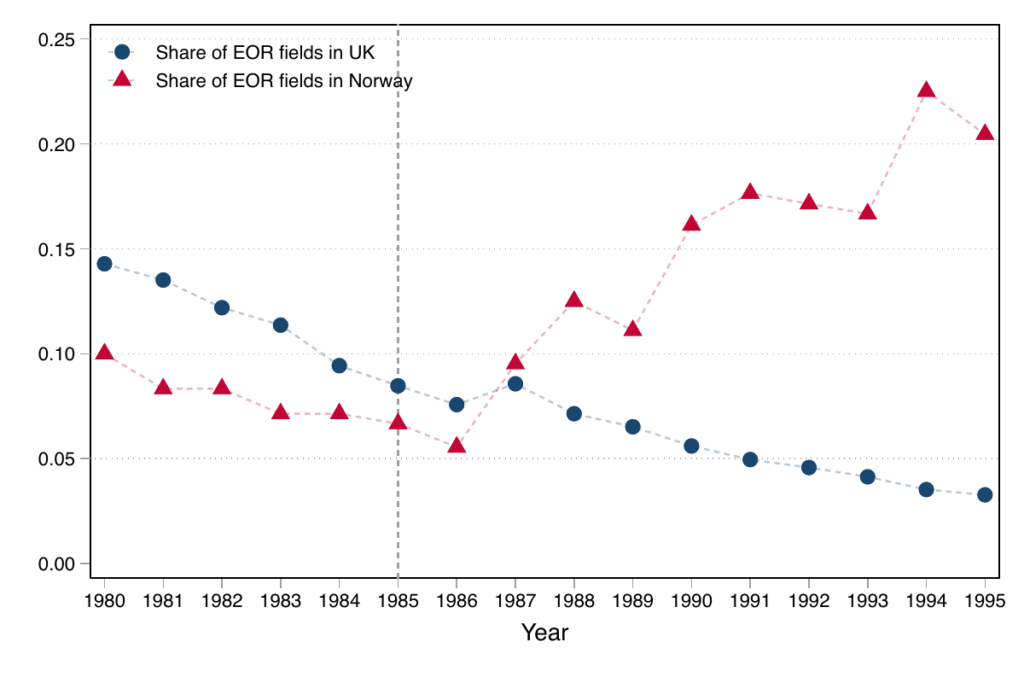

In practice, both governments repeatedly reopened contracts. The U.K. passed the Oil Taxation Act of 1975 and the Petroleum and Submarine Pipelines Act of 1975, which retroactively modified the “Model Clauses” of existing licenses; further changes followed in the 1980s. Norway, for its part, amended the Continental Shelf Act in December 1972 to impose quarterly royalty payments and a graduated 8–16% royalty rate, pointedly refusing to exempt pre-1972 licenses—the move that would ultimately trigger the Phillips Petroleum lawsuit. Combined with the softening of oil prices in the early 1980s, this persistent legal uncertainty eroded investment incentives in both jurisdictions. Enhanced Oil Recovery adoption was already trending downward in both countries by the early 1980s, as Figure 1 shows.

That changed on December 19, 1985. In Phillips Petroleum v. The State, the Norwegian Supreme Court declared that the government could not unilaterally alter the terms of existing petroleum licenses. The ruling anchored sovereign commitment in constitutional law, making retroactive interference far more costly for the state. The U.K., meanwhile, continued to revise license terms at will. As Figure 1 shows, the divergence was immediate: large irreversible investments surged in Norway after the ruling, while the U.K. continued its decline.

Figure 1: Share of fields adopting Enhanced Oil Recovery in Norway and the UK. After the 1985 ruling, Norwegian adoption surged while UK adoption continued its decline.

In our study, we focus on Enhanced Oil Recovery (EOR)—a mature oil extraction technology—as our measure of investment. EOR, which injects chemicals into aging fields to extract residual reserves, was the sole technology at the time that could not be reversed (its costs recuperated) once implemented, had long payback periods (10 years for EOR vs. two years for shale drilling, for instance), and maintained high asset specificity (equipment could not be redeployed easily to other assets). These features made EOR adoption highly sensitive to whether firms trusted the fiscal environment to remain stable. This contrasts with a short-cycle, low-investment industry like shale. Studies show that despite Argentina’s weak contract enforcement record, the country’s oil and gas industry has boomed because of shale’s short-cycle nature of a two-year payback and low investment requirement. These smaller-scale conditions limit the risk of sovereign hold-up.

Crucially, whether a given field is suitable for EOR is a matter of geology, not management. Reservoir size, depth, porosity, permeability, oil viscosity, and sulfur content—together with the platform’s drive mechanism—determine technical eligibility. In our sample, roughly 35% of active fields in the two countries during this period met the engineering criteria for EOR, out of a total of 521 North Sea fields. This cross-field heterogeneity is what gives our research design its traction. Moreover, EOR was widely available through service companies like Halliburton, so adoption did not require inventing anything new.

Credible commitment unlocked innovation

Using granular data covering every field and licensee in the North Sea from 1975 to 1995, our empirical strategy compares firms with similar pre-1985 portfolios but differing geographic exposure to the ruling. Consider two firms with comparable North Sea portfolios: one holds most of its EOR-eligible fields on the Norwegian side of the border, the other on the British side. The 1985 ruling raised the expected returns of EOR investment for the first firm, while leaving the second’s incentives unchanged. We call a firm “more exposed” to the ruling when a larger share of its pre-1985 portfolio sits in Norwegian EOR-eligible fields.

The results are striking. Firms holding a 10-percentage-point larger share of Norwegian EOR-eligible fields in their pre-1985 portfolios—our “exposed firms”—were 3.5 percentage points more likely to adopt EOR, nearly doubling their adoption rate. They increased production by 38% and gained 39% more market share in the North Sea. Crucially, these market-share gains did not come from pure zero-sum displacement. We find no evidence of crowding-out: non-EOR firms did not lose output, and production in Norwegian non-EOR-eligible fields remained stable. Instead, exposed firms expanded along two margins. At the intensive margin, they consolidated ownership in Norwegian EOR-eligible fields by buying out passive co-owners, raising operator ownership shares by 27 percentage points and top-three concentration by 40 percentage points. At the extensive margin, they acquired about one additional field on average (against a baseline portfolio of 7.8 fields), with 56.5% of these acquisitions in EOR-eligible geologies. In short, they grew by putting capital and expertise to work on fields that had previously been underdeveloped because sovereign hold-up risk had deterred the required irreversible investment.

Both private and state-owned firms operate in the Norwegian market. State-owned Statoil, established in 1972, enjoyed substantial statutory advantages: a “carried interest” under which exploration costs were borne by other licensees, and a “gliding scale” allowing it to claim up to 80% equity at production. One might therefore expect state-owned firms to have been insulated from sovereign hold-up risk. They were not. Before 1985, state-owned firms in Norway invested cautiously in EOR alongside private firms—a sign that even direct government backing did not neutralize the concern that contractual terms could be rewritten. After the ruling, both state-owned and private firms with EOR expertise gained market share, but the most aggressive portfolio expansion and diversification came from private firms with preexisting operational experience in EOR—Conoco, Mobil, and Shell. These firms had accumulated operational know-how through hands-on experience with EOR. Once sovereign hold-up risk was reduced, that underused expertise could be deployed more productively: they acquired 4.7 new fields per 10-percentage-point exposure (versus 2.8 for state-owned firms with similar expertise) and ventured further into geologically challenging territories. Figure 2 illustrates one consequence: after the ruling, Norway sharply accelerated investment in geologically challenging fields—heavy oil, sour oil, and deep wells—that had previously been avoided.

Figure 2: Investment in high-risk fields (heavy oil, sour oil, deep wells) in Norway and the UK. After 1985, Norway accelerated development of geologically challenging fields.

The pattern is consistent with transferable know-how. Firms that had learned to operate EOR in one field leveraged that expertise to diversify into technologically related domains. Their diversification was more concentrated in other extraction technologies—such as primary and secondary recovery methods that can be used at earlier stages of an oil and gas field’s life cycle—that share technical features with EOR. This is exactly what a model of cumulative, firm-specific learning would predict: knowledge decays with technological distance, so firms diversify into adjacent capabilities first.

A global problem hiding in plain sight

One might think that sovereign hold-up is a problem confined to weak states or developing economies. Our evidence suggests otherwise. Norway and the U.K. are among the world’s most stable democracies, with strong rule of law and sophisticated regulatory frameworks. Yet even in this setting, the credibility of sovereign commitment had large, measurable effects on technology adoption and industry structure.

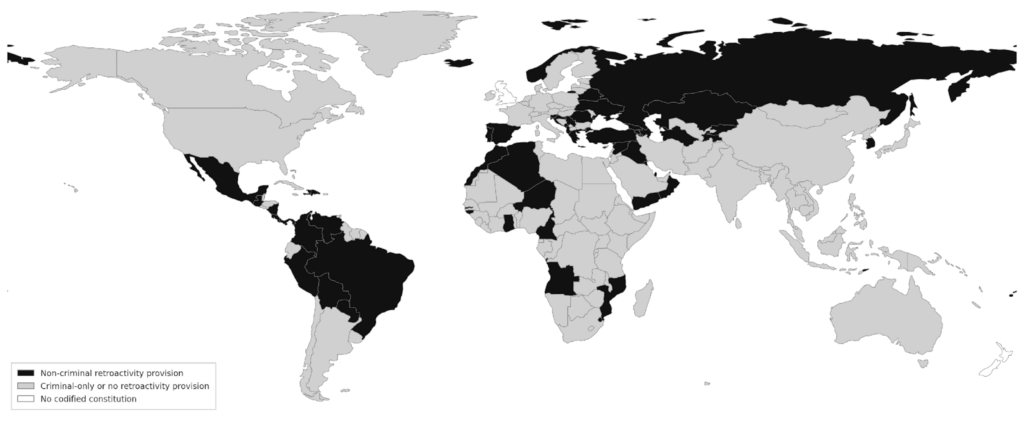

To find out how widespread this problem is, we conducted a comprehensive survey of national constitutions, using a large language model-assisted coding procedure to classify whether constitutions explicitly prohibit retroactive legislation beyond the criminal sphere. The answer, shown in Figure 3, is sobering.

Figure 3: Countries with constitutional prohibitions on non-criminal retroactive laws (shown in dark). Only 30.6% of codified constitutions contain such protections. Countries in white (Israel, New Zealand, U.K.) lack codified constitutions.

Only 30.6% of the world’s codified constitutions explicitly prohibit non-criminal retroactive legislation. Among countries in the Organization for Economic Co-operation and Development with codified constitutions, the figure is only slightly better: just 11 out of 35 have such protections. The vast majority of countries—including many with large, capital-intensive industries—leave firms exposed to the risk that the state will rewrite the rules after investments are made.

Policy implications

Our findings carry lessons beyond the oil patch. Any long-horizon investment—in infrastructure, the energy transition, or public procurement—depends on the stability of administrative and fiscal regimes. When governments retain the discretion to alter terms retroactively, firms rationally discount the expected returns from irreversible commitments. The result is not just less investment, but less learning, less technological diversification, and less innovation.

The Norwegian experience suggests that constitutional constraints can function as a powerful form of industrial policy—not by directing resources toward specific sectors, but by making the state’s promises credible. By tying the government’s hands, the 1985 ruling transformed promises into commitments, unlocking a trajectory of technological deepening that benefited both firms and the broader economy.

But constitutional text alone is not enough. Even where prohibitions on retroactivity exist, enforcement depends on judicial interpretation. Tax law is a canonical example: courts routinely weigh retroactive fiscal measures against public-interest considerations. Beyond constitutional entrenchment, sovereign commitment can also be secured through delegation to independent agencies, international legal frameworks, or constitutional fiscal rules.

The broader lesson is that credibility of commitment is a distinct and measurable determinant of economic performance—one that can be separated from general institutional quality. Getting it right does not require reinventing governance. It requires making existing promises stick.

Authors’ Disclosures: The authors did not receive financial support from any firm or person for this article or from any firm or person with a financial or political interest in this article. The authors report no conflicts of interest. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.