In new research, Vishavdeep Sharma and Krishnendu Ghosh Dastidar analyze corporate corruption through the lens of market competition. Firms often bribe officials to block rivals from entering their markets, and their incentive to do so depends less on how competitive a market is than on what kind of competition it has.

Corporate corruption is usually treated as a problem of weak institutions or lax enforcement. That view is correct but incomplete. In many markets, corruption is also a competition problem.

Incumbent firms can benefit from corruption by lowering regulatory costs or purchasing preferential treatment to, for example, procurement. Consequently, corruption can make it harder for potential rivals to compete. Corruption aimed more intentionally at keeping potential competitors out of the market can also raise the operating costs of a potential rival, delay business approvals, restrict access to key inputs, or create regulatory obstacles that protect the incumbent’s market position.

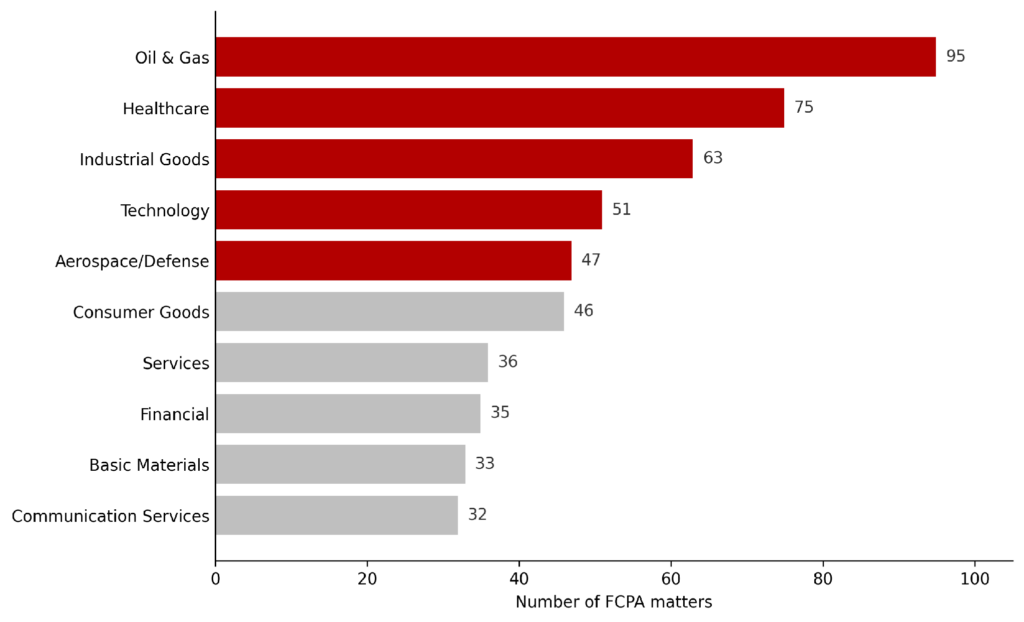

Corruption as a barrier to entry is particularly relevant in regulated sectors with concentrated markets, where firms frequently interact with government officials. Figure 1 illustrates the distribution of United States Foreign Corrupt Practices Act (FCPA) enforcement cases across industries, with prominent sectors including oil and gas, healthcare, industrial goods, technology, and aerospace/defense: areas where regulation plays a key role in market access. Not every FCPA case is about deterring entry by a rival, but the pattern shows that corruption clusters where market power and regulation matter most.

Figure 1. FCPA enforcement matters since the statute’s enactment (1977), by industry (top 10). Red bars mark the top five industries with the most FCPA enforcement matters. Source: Stanford Law School FCPA Clearinghouse.

Corruption to block entry

Consider how corruption plays out where market entry itself is the prize. In India, the allocation of 2G telecom spectrum and coal mining concessions became two of the country’s largest corruption controversies. The reason was simple: licenses and coal blocks were selectively handed out by the government, not won. In 2012, India’s Supreme Court cancelled 122 telecom licenses, and in 2014, it cancelled more than 200 coal block allocations. In both cases, it found the allocation process illegal and unconstitutional. The pattern is not unique to India. In 2019, Walmart paid more than $280 million to resolve a U.S. enforcement case over payments made to expedite the obtainment of store permits and licenses in countries including India, Brazil, China, and Mexico.

In these cases, firms competed not just in the product market, but for the right to be in it at all. These cases cluster in capital intensive sectors like defense, energy, and infrastructure, which sit atop the FCPA chart in Figure 1, and where capacity and access to scarce resources decide who wins. Competition law generally recognizes entry barriers when assessing market power, but corruption and competition are usually handled by different authorities. In the U.S., the Justice Department and the Securities and Exchange Commission pursue bribery under the FCPA, while the Federal Trade Commission and the Justice Department’s Antitrust Division police market power. One asks whether a payment was legal. The other asks about market structure.

Modeling competition and bribery incentives

Corruption can harm competition, but does a more competitive market reduce the incentive of a dominant firm to bribe government officials? More competition reduces profits, limits market power, and weakens the rewards from protecting a privileged position. Our research shows that competition does reduce corruption, but the correspondence is nuanced. The incentive to bribe depends not only on how competitive a market is, but also on how firms compete.

In our paper, “The Optimal Bribe: Price Versus Quantity Competition in Oligopolies,” published in The Manchester School, we extend Krishnendu Dastidar and Makoto Yano’s model of an incumbent firm facing a potential entrant. The incumbent can pay a bribe that raises the entrant’s costs to enter the market. The entrant must decide if the costs make entry still worthwhile. If entry occurs, the firms compete in a market where goods are differentiated by price, quality and brand.

The key comparison is between two common forms of oligopolist competition between a few firms: by price or by quantity and capacity. Retail and consumer electronics compete largely by setting prices to win customers. Oil and gas, cement, and electricity generation firms compete mainly by setting output or capacity (production volumes, plant capacity) rather than price. These two forms of competition can generate very different incentives, even when the underlying market looks similar.

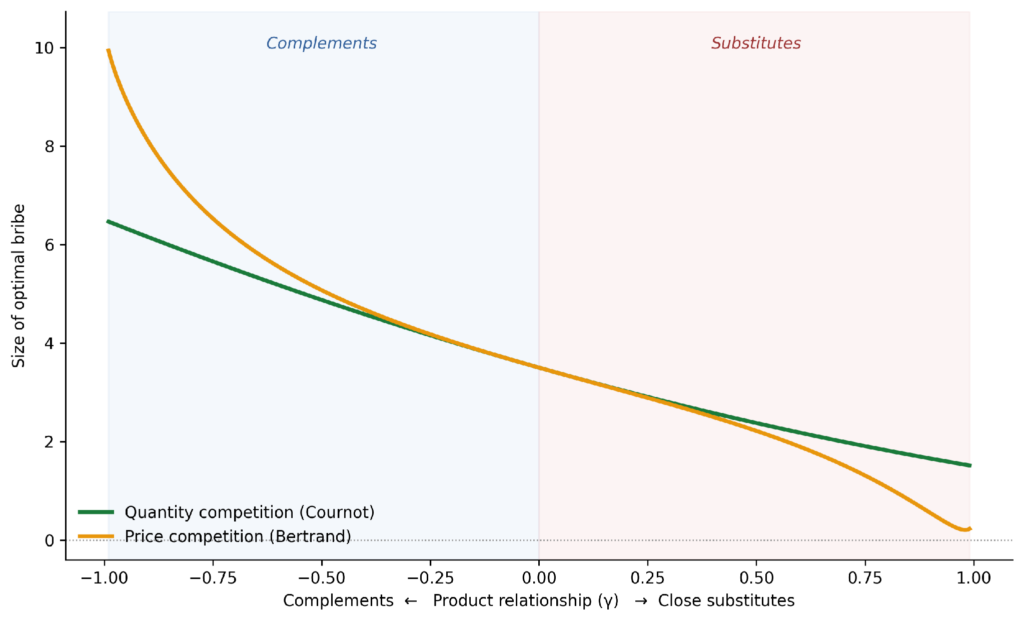

Our main result is that when the incumbent’s and entrant’s products are substitutes, the optimal bribe is lower under price competition than under quantity competition. However, when the products are complements, this ranking can reverse. Figure 2 illustrates this result.

Figure 2. Optimal bribe required to deter entry, by product relationship (γ) and form of competition. Source: Authors’ simulation, (Sharma and Dastidar 2026).

The intuition is straightforward. If an entrant is threatening to enter a market with a good or service that is a close substitute to what the incumbent firm offers, it can attract consumers by cutting prices, forcing the incumbent to respond. This compresses profits. However, if the market is already competitive and pushing down prices, the incumbents have less to gain from paying a large bribe to block another firm from entering the market. Bribery becomes a less attractive investment.

Under quantity competition, the situation is different. Firms adjust quantities rather than directly undercut each other’s prices. Because each firm accounts for how its own output lowers the market price, firms hold back output, so prices and profits stay higher than under price competition. Competition is thus often softer, and incumbents can retain higher profits even in the presence of rivals. Because there is more profit to protect, the incumbent may be willing to pay more to deter entry. This is why bribery-based entry barriers can be higher under quantity competition when goods are substitutes.

The result changes when the products are complements. In such markets, the entrant’s product may expand demand for the incumbent’s product rather than simply stealing demand from it. Even so, the incumbent does not welcome entry. Under Bertrand competition, firms’ prices are strategically interdependent, so once the entrant is in, the incumbent can no longer set price independently to fully exploit demand for its product. The entrant enhances demand for the incumbent’s product, but price competition prevents the incumbent from capturing that enhanced demand at its preferred price, so the profit lost to entry is large and deterrence is valuable. Hence, for complements, the optimal bribe is higher.

The broader lesson is that corruption incentives are not determined only by enforcement intensity or the quality of political institutions. They are also shaped by market structure. An incumbent’s willingness to bribe depends on the profits it expects to preserve by keeping rivals out. Those profits depend on whether firms compete through prices or quantities, and on whether products are substitutes or complements. This connects to a wider literature on how corruption shapes market quality and entry in emerging economies, where weak competition and weak institutions often reinforce one another.

Policy implications

The link between corruption and competition has policy implications. Anti-corruption and competition policy are usually treated separately, yet our analysis suggests they are closely connected.

This link is not just academic. When the U.S. government paused FCPA enforcement in early 2025, it argued that strict anti-bribery rules could disadvantage American firms competing abroad. Whatever one makes of that argument, it rests on a revealing premise: that how bribery is policed affects a firm’s competitive position. Krishnendu Dastidar and Makoto Yano examine exactly this tension, analyzing how anti-bribery enforcement shapes market quality and competition in emerging economies. Our analysis adds what the debate leaves out. The return on bribery also depends on whether firms compete on price or quantity, and whether the entrants’ products are substitutes or complements.

A bribe that raises a rival’s cost is not only a corruption problem. It is also a market-power problem. It can protect incumbents, reduce entry, and weaken competitive pressure. This is why regulators should pay attention to sectoral differences. In sectors where products are close substitutes and price competition is intense, bribery may be less attractive as an entry-deterrence tool. In sectors where quantity competition, complementary goods, procurement constraints, or regulatory bottlenecks dominate, bribery may be a stronger mechanism for protecting incumbents, and regulators should consider it a more serious threat.

For policymakers in developing economies, this reframes a familiar debate. Efforts to ease entry into markets—through transparent auctions, time-bound regulatory approvals, and reduced administrative discretion—are usually defended on efficiency grounds alone. But they also serve as anti-corruption measures. By making entry more contestable and competition more price-based, such reforms directly lower what an incumbent stands to gain from keeping rivals out, at least where goods are substitutes, and so lower what a bribe is worth.

The point is not that price competition eliminates corruption, nor that quantity competition always increases it. What changes is the return to corruption. Entry barriers are not always visible in laws, tariffs, or formal regulations; sometimes they are created through informal payments that raise rivals’ costs. Enforcement should therefore ask not only whether a payment was illegal, but what market position it protected. Corruption policy needs market analysis. To know when firms are likely to bribe, ask what happens after entry.

Author’s Disclosure: The authors report no conflicts of interest. You can read our disclosure policy here.

The views reflected in this research project do not necessarily reflect the views of the Federal Reserve Bank of Richmond, the Federal Reserve Board, or the Federal Reserve System. Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.