")

A forgotten aspect of the New Deal is that it took place amid inflation and rising prices. Contemporary debates over inflation and whether corporate greed has a role in driving price hikes echo similar debates during Roosevelt’s second term, as enforcers attempted to push against rising prices by curbing monopoly power while maintaining purchasing power.

“There is real danger of runaway prices … Then, unless firm action is taken, will come the race between purchasing power and inflated prices – a losing race since purchasing power can not keep up.”

“Many of these prices are being deliberately raised by monopolistic devices.”

“Some of the price rises are due to monopolistic practices, and some are due to shortages of supplies.”

The above quotes may appear to have come out of this year’s debates over inflation, as many Americans are finding their paychecks in a losing race against price increases. There is debate and uncertainty about the causes. Some argue that this inflation is driven by overheating and increased purchasing power. Others argue it is supply chain disruptions from Covid-19, and yet others maintain that corporate greed is driving unjustified price hikes. The comments above were written, however, in 1937, by an advisor to President Franklin D. Roosevelt, as the United States found itself in a very similar situation. As Covid has today, the Great Depression of the 1930s created one of the largest economic disruptions of supply, employment, and output in the nation’s history. In both cases, millions were put out of work, supply-chain shocks and shortages limited recovery, and massive government spending propped up key sectors of the economy.

There are some less-appreciated similarities central to today’s debates. Just as the public’s attention is focused on inflation, a forgotten aspect of the New Deal is that it took place amid inflation and rising prices. Furthermore, in both cases—1937 and 2022—for decades prior the American government had been supporting the ability of powerful companies to collectively set their own prices to ensure their profits. In the 1920s, the Federal Trade Commission (FTC) had supported trade associations in their attempts to limit output, set common wages, and at the extreme, entirely undermine competition to fix prices, along with corporate-friendly court decisions. This was capped off by an attempt in the early 1930s under the National Recovery Administration (NRA) to allow industries to cartellize under government supervision, and many of these cartel-like controls lasted through the 1930s.

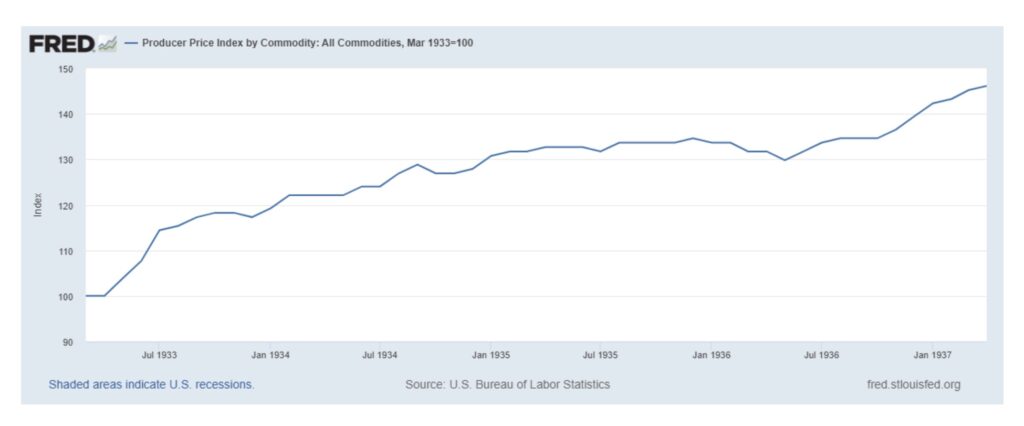

This set of policies led to price increases during the 1930s—shown above via the producer price index up to this moment in 1937—paradoxically even as output remained deeply depressed and unemployment persistently high, and much of the country was still struggling. Researchers today have identified the price-fixing permissions of the NRA as a central explanation for rising prices during the 1930s even after the NRA experiment ended in June 1935, and as a central reason why the Depression dragged on for so many years. So in 1937, when prices suddenly spiked even faster, several Roosevelt advisors—including Henderson, Robert Jackson, Felix Frankfurter, Thomas Corcoran, and Benjamin Cohen—argued that these monopolistic practices were the driver of many price increases and, if nothing was done, could hold back recovery or cause another recession.

Similarly, since the 1980s, American courts and regulatory agencies have supported the ability of powerful corporations to merge, monopolize, collude to fix prices, exclude or control other companies, and push down wages. Beginning in the 1970s and 1980s, a new way of thinking about antitrust came into fashion, favoring mergers as supposedly efficient and seeing little risk in allowing industries to consolidate. To sum up this attitude, Justice Scalia decided in 2003 that “The mere possession of monopoly power, and the concomitant charging of monopoly prices, is not only not unlawful; it is an important element of the free-market system. The opportunity to charge monopoly prices—at least for a short period—is what attracts ‘business acumen’ in the first place; it induces risk taking that produces innovation and economic growth.”

The purpose of the antitrust laws had now become, in part, to preserve monopoly.

As in the 1930s, these changes have increased prices across the American economy, but until now, not very clearly or noticeably. Before this past year, these price increases were slow, creeping, and imperceptible over decades. Nonetheless, researchers comparing the United States to other wealthy countries estimate that, even before the pandemic, American households have been paying $5,000 more per year for basic goods and services than if markets were more competitive. Average markups—the difference in price between the production cost and sales price—have risen from 21 percent to 61 percent over marginal cost since 1980.

Real as they were before, now these price increases are less subtle. As the recovery from Covid-19 runs into inflation, price increases reflect a combination of genuine supply shocks as well as obvious price hikes from powerful firms with a history of price-fixing. Taking advantage of both their bargaining position and consumers’ ignorance about the true scale of cost increases, major firms have been increasing prices well beyond their cost increases, bragging loudly about it on earnings calls, and explaining that their market power allows them to do this, whether in industries like beverages, meatpacking, or even PPE critical for Covid mitigation.

Despite this, most economic experts are adamant that little or nothing is amiss here. A recent expert survey panel of US economists by Chicago Booth’s Initiative on Global Markets regarding inflation and market power shows this attitude well, with responses including, “The proposition is an elementary confusion of levels and changes–market power causes high prices, not rising prices,” “It is demand and supply,” and, “I don’t see the logic: U.S. markets have been concentrating for decades but high inflation is [less than] one year old.” Similarly, when asked about whether antitrust could play a role in controlling inflation, the same survey of economists responded that “Antitrust actions take a long time to implement,” “Even if excessive monopoly power was a contributing factor, antitrust couldn’t act that fast,” or that the government “couldn’t even get the case filed in 12 months.”

Having decided that market power is not responsible for inflation, or that antitrust would take too long, the conclusion appears to be instead to do nothing: since it is just supply and demand, leave it be. However, inaction leaves the policy response to inflation in the hands of the independent Federal Reserve, whose one policy lever is to raise interest rates to control inflation by reducing workers’ bargaining power and wage gains, based on the theory that inflation is driven by excess purchasing power. It should be noted that wage gains cannot be driving inflation, as prices are rising faster than wages, but on the basis of this logic the Federal Reserve raised rates on March 16 nonetheless.

“the debate between corporate greed and purchasing power is not just a technical one. It is a question of values. Who should bear the burden of adjustment: workers or powerful corporations?”

However, the debate between corporate greed and purchasing power is not just a technical one. It is a question of values. Who should bear the burden of adjustment: workers or powerful corporations? Inaction in this case is to take a side, and that side is to control inflation by preventing workers from having as much money to buy things, and ensuring that major corporations are free to maintain their unprecedented and inflated profit margins. In a country where the share of income going to workers (rather than owners of capital) has been falling for a generation, and where recently a huge fraction of Americans were put out of work through no fault of their own, there is a normative judgment implicit in concluding that massive profits from high prices are natural according to abstract laws of supply and demand, but that inflation needs to be controlled by restraining workers’ incomes.

But alternatives exist, as this was not the approach taken in 1937. Short term solutions to high prices and monopoly could be faster and more practical, as Henderson’s New Deal approach reveals: “The government could let it be known that it was attacking the threat of high cost of living by attacking the monopolies which are raising prices, thus endangering further recovery. Publicity, publicity, and more publicity would check controlled price rises until positive checks could be established.” Robert Jackson, Roosevelt’s Assistant Attorney General for antitrust, did just that by going on a series of speeches in the fall of 1937 attacking large corporations for holding back recovery through monopolistic price increases. Proposals for faster results exist today as well. For example, one proposal from economist Hal Singer suggests launching automatic antitrust investigations into any concentrated industry with a significant price hike, a penalty that would certainly help deter recent price gouging.

More generally, for the Roosevelt Administration in the 1930s, parsing the distinction between supply shocks, purchasing power, and monopoly was less important than using all the tools available. In his proposal to Roosevelt, Henderson wrote that “it would seem logical to try to affect supply and demand and also to work vigorously against controlled prices.” The plan was to “move in with all the executive and legislative powers and fight along the whole front to keep prices down and buying power up.” “At the same time it was hammering prices at the top, [the government] could sustain purchasing power with adequate relief” through minimum wages, income support, and cheap money through monetary policy.

This push against rising prices and monopoly power helped to reinvigorate the New Deal after its struggles early in Roosevelt’s second term. The FTC had already been receiving around 500 complaints per month regarding high prices or price-fixing, several times its usual caseload. In the summer of 1937, the Depression worsened again amid steady price increases for many products and commodities. Requests for investigations about these price increases came in from former FTC Commissioners, the Treasury, the Department Agriculture, and private citizens. The ensuing investigations were centralized into one FTC investigation by the end of 1937, resulting in a 700-page report that found anticompetitive, controlled prices in most industries examined. With detailed information on price-fixing and monopoly control in many industries, the Department of Justice launched a 10-year trustbusting campaign to rein in dominant corporations and reverse the policies that had given them so much power.

President Biden had already taken some of the actions above, taking a “whole-of-government” approach to gathering information, proposals, and public comment, with a dedicated committee to examine the contemporary monopoly problem. Aggressive enforcers, Jonathan Kanter and Lina Khan, have been put at the helm of the Department of Justice’s Antitrust Division and the FTC. Yet hesitation remains within the White House and in Congress, in the face of opposition from professional economists and business concerns, to pursue this agenda further. Not only are the alternative options misguided, but antimonopoly policies and politics are not a narrow question around economic technicalities. They are a statement of our priorities as a country. The US has seen this mix of price increases, corporate profiteering, and an uncertain economic recovery before—the last time they faced this predicament, Americans did not leave their fate in the hands of corporate masters.

Disclosure: Dr. Peinert has previously received research funding from the Economic Security Project’s Antimonopoly Fund.

Learn more about our disclosure policy here.