The green transition is faltering in both advanced and developing economies. While politics and market risk is stalling private investment in clean energy in advanced economies, an imbalanced global value chain is preventing investment in clean energy in developing countries, write Piergiuseppe Fortunato and Verena Hitner Barros.

The global energy transition is often framed as a technological race against time. Over the past decade the cost of solar power, wind energy, and batteries has fallen dramatically. In many parts of the world, renewable energy is now the cheapest source of new electricity. Electric vehicles are scaling rapidly. Clean technologies are spreading faster than most analysts predicted only a few years ago.

Yet, global emissions are not declining at the pace required to meet our climate targets. Despite unprecedented technological progress, the world remains far from a trajectory to keep global warming below 1.5 degrees celsius of pre-industrial levels, consistent with the 2016 Paris Agreement. Figure 1 makes this tension visible: clean energy costs have fallen sharply, and installed capacity has expanded rapidly. Yet, deployment remains far below what a 1.5°C-consistent pathway would require.

Figure 1. Falling renewable costs and rising capacity—but still off a 1.5°C pathway.

The reason is that the energy transition is not just a problem of technological innovation. It is, first and foremost, a question of political economy. Today’s energy transition is also a development transition. And unless the global distribution of industrial capacity, technological control, and value creation changes, decarbonization will remain slower, more fragile, and more costly than climate goals require.

Why clean energy investment is faltering in developed countries

The fact that clean technologies have become cheaper does not automatically translate into sufficient investment. What ultimately drives private investment decisions is not the marginal cost of energy but expected profitability.

Energy systems are embedded in industrial, financial, and regulatory structures built around fossil fuels. Liberalized electricity markets in many countries generate high price volatility and uncertain returns, discouraging long-term investment. As a result, even as renewable technologies become more competitive, private investment continues to lag behind what would be required to meet global climate targets.

This gap reflects institutional and structural constraints rather than technological ones, and it is shaped by how markets are organized, how risks are distributed, and how returns are guaranteed across different segments of the global economy.

Major economies have sought to reduce these constraints through renewed industrial policies. The United States, the European Union, and China have each launched large-scale industrial strategies aimed at securing leadership in batteries, electric vehicles, renewable equipment, and emerging technologies such as green hydrogen. These policies have helped to incentivize private investment in some countries. For example, the U.S. Inflation Reduction Act has triggered a surge in announced investments in battery manufacturing and electric vehicle supply chains, while China’s long-standing industrial strategy has enabled the rapid scaling of solar and battery production.

However, the private sector has failed to respond to industrial policy in these countries and regions for several reasons, often because policy frameworks lack credibility or coordination. In parts of Europe, regulatory fragmentation and volatile power prices have slowed investment despite large policy commitments.

Furthermore, political uncertainty is also starting to weigh on the transition. The resurgence of political platforms more hostile to climate regulation, both in the U.S. and parts of Europe, has cast doubt on the durability of incentives and policy support. In capital-intensive sectors with long time horizons, credibility matters as much as technology. When policy signals weaken, investment hesitates. Recent evidence points to delays and cancellations in clean energy projects, particularly in offshore wind, where over the past few years hundreds of gigawatts of planned capacity have been postponed or scaled back amid rising costs and regulatory uncertainty.

Financial markets reflect the same shift. Major asset managers such as BlackRock have begun to recalibrate their ESG strategies, reducing the prominence of climate commitments, scaling back participation in collective climate initiatives, and adopting a more cautious stance toward new green investments. This repositioning reflects not only changing market conditions, but also growing political backlash and regulatory uncertainty, which are making long-term climate-aligned strategies more difficult to sustain.

Why clean energy investment is failing to reach developing countries

Advanced economies and China possess the fiscal space, the technological base, and the institutional capacity to support large-scale green industrial strategies. Many developing economies do not. High debt burdens, limited fiscal resources, and tighter financial conditions constrain their ability to subsidize investment, build infrastructure, or support domestic industries. In countries such as India and South Africa, these constraints have translated into lower expected returns and higher risks from clean energy projects, discouraging long-term investment.

As a result, the emerging global green economy is developing within a highly uneven landscape. Production may be spreading geographically, but because the major economies are treating the green transition as a strategic industrial domain, they are limiting what technological and manufacturing innovations are distributed to other countries part of the global production chain. This limits developing countries’ ability to build their own green industries and attract investment in their clean energy infrastructure. The transition is global in scope but asymmetric in structure.

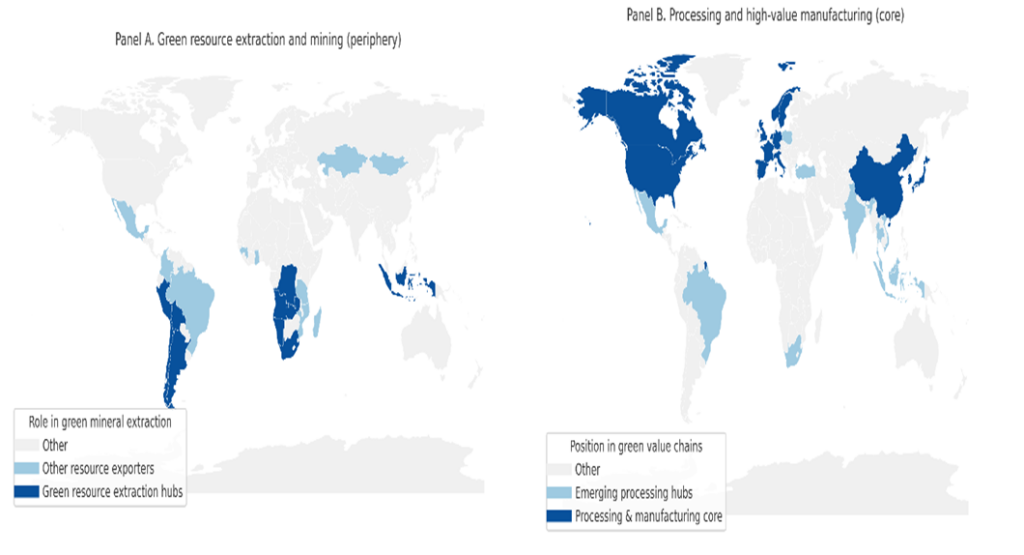

Figure 2 illustrates this asymmetry across critical minerals: extraction is concentrated in the Global South, while refining and higher value-added processing are dominated by China and advanced industrial economies. The green transition is not flattening industrial geography but reorganizing it along updated lines of hierarchy.

Figure 2. The unequal geography of the green transition.

These asymmetries are particularly visible along global value chains. The production of clean technologies relies on complex international supply networks that span extraction, processing, manufacturing, and assembly. Different segments of these chains capture very different shares of value.

Countries specializing in high-value segments (advanced manufacturing, technology design, and capital-intensive production) capture a large share of profits and technological rents. Countries specializing in extraction or lower value-added manufacturing capture much less. Empirical evidence from global value chain data shows that upstream, resource-based activities often account for a relatively small share of total value added (typically on the order of 10–20 percent) while downstream manufacturing, branding, and distribution capture the bulk of value.

This unequal distribution of value and control has direct implications for the pace of decarbonization. When most value, technology, and decision-making power are concentrated in a small number of countries and firms, incentives to invest in clean technologies become fragmented across the system. Countries specializing in extractive or low-value segments often have limited fiscal capacity and weaker incentives to invest in costly clean technologies. Countries capturing higher rents can externalize part of their emissions along the supply chain.

The result is a structural misalignment between who bears the environmental costs of production and who controls technological and investment decisions.

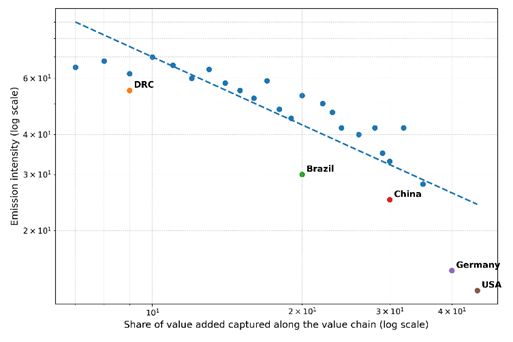

Figure 3 illustrates this dynamic. Across countries, there is a systematic relationship between the share of value captured along global value chains and the carbon intensity of production. Countries capturing a larger share of value tend to generate fewer emissions per unit of value added, while countries capturing less value tend to host more carbon-intensive stages of production. This pattern suggests that the organization of global production itself is shaping the geography of emissions.

Figure 3. Value captured along global value chains and carbon intensity of production

Trade reinforces this dynamic. Many advanced economies have reduced territorial emissions over the past two decades while increasing imports of carbon-intensive goods produced elsewhere. A significant share of global emissions is now embedded in traded goods. Estimates suggest that around 20–30% of global CO₂ emissions are linked to international trade. As a result, production-based emissions have declined in some countries even as consumption-based emissions remain substantially higher. Emissions are not disappearing, they are being redistributed across the global economy.

Without a more balanced distribution of industrial capabilities and technological capacity, this structure risks slowing the global pace of decarbonization. Emissions reductions achieved in one segment of global value chains may be offset by expansions elsewhere. The transition becomes less coordinated, more costly, and politically more fragile.

Industrial policy and strategic space in the Global South

Developing economies are not merely passive participants in this process. Many are experimenting with policies designed to reshape their position within global value chains. Public development banks, strategic procurement, local-content requirements, and targeted industrial policies are being used to build domestic capabilities in renewable energy, batteries, and green manufacturing.

Brazil’s recent industrial strategy, Nova Indústria Brasil, illustrates this effort. The program combines long-term public finance, technology missions, and sectoral planning to rebuild industrial capacity and position the country within emerging green value chains. Its objective is not simply to decarbonize, but to use the transition as a lever for structural transformation. Such initiatives highlight a central point: the key challenge for developing economies is not to replicate the fiscal scale of the U.S., China, or the EU, but to identify strategic segments where domestic capabilities can be developed and value capture expanded. Industrial policy can create space for upgrading even in a constrained global environment.

However, national strategies alone face limits. Fragmented markets, high capital costs, and externally determined technological standards constrain what individual countries can achieve. Regional coordination and new forms of international cooperation will be essential to expand fiscal space, share technological capabilities, and support long-term industrial investment. Emerging initiatives point in this direction. In Latin America, efforts to strengthen regional value chains around lithium and battery production are beginning to explore coordinated strategies for upgrading production. In Africa, the African Continental Free Trade Area (AfCFTA) is creating a framework to support regional value chains and industrial upgrading, including in energy and manufacturing sectors.

Decarbonization as a development challenge

Developed economies and China face unique challenges of incentivizing private sector investment and adoption of clean energy. Several European countries and the U.S. face the additional problem of political antagonism toward clean energy.

The rest of the world faces a different set of issues that will stymie decarbonization convergence: existing market and geopolitical structures that risk reinforcing existing hierarchies in new technological forms. A small number of countries may capture the bulk of technological rents and industrial capacity, while others remain locked into lower value-added and more carbon-intensive segments of global production.

Decarbonization is therefore not only an environmental challenge or question about market risk. It is also a structural development challenge. Its success will rely not only on technological innovation but on how value, investment, and industrial capabilities are distributed across the global economy. Clean energy technologies are spreading rapidly. But unless the geography of value creation shifts as well, the transition may proceed more slowly and unevenly than climate goals require.

Authors’ Disclosures: The views expressed are those of the authors and do not necessarily reflect those of their respective institutions. The authors report no conflicts of interest. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.