Increasing concentration is not unique to the US—recent studies show that concentration is rising in Europe as well, although to a lesser extent than in the US. Is concentration rightly measured? And what are its driving forces? Barriers to entry, one of the most formidable sources of market power, appear to matter most.

Who does Boeing compete with? If you read academic research, thousands of firms compete in the US aircraft space/aircraft manufacturers industry. If you were to ask Delta Airlines, a potential consumer of Boeing planes, it depends on what they are shopping for. If they are shopping for planes that carry many passengers a long way, the answer would be Airbus. If they are shopping for a plane that carries 100 people a relatively short distance, Boeing would not even be on the list of options. Point being: the definition of the market matters. It matters especially when you try to measure the level of market concentration, a debate that in recent years has been at the top of the policy agenda.

In March 2017, the Stigler Center hosted a three-day conference on the question of concentration in the US economy. During the opening panel, economists mostly agreed that existing evidence highlights the problem of concentration in the US. These dynamics are worrisome, because increased concentration “drives up prices while driving down investment, productivity, growth, and wages, resulting in more inequality,” as suggested by Thomas Philippon. Since then, debates on the rising trends of market concentration, markups, and profits, as well as the declining shares of labor and investment, continue unabated. Evidence demonstrates that all this is not unique to the US, with many countries and sectors around the world affected by similar trends. Importantly, prominent work by OECD economists shows that concentration is also increasing in Europe, although to a lesser extent than in the US.

Because of data limitations, almost all existing studies measure concentration aggregating firm balance sheet data using industry classifications, mostly at the national level. This is problematic, since this aggregation does not correctly reflect the competitive interactions among firms. A market is a set of competing products located in certain geographic areas that are substitutes of one another. In antitrust law, this is called a relevant product and geographic market. This stance is reflected in the US Horizontal Merger Guidelines, as well as in the EU Commission’s Horizontal Merger Guidelines. This is not a mere technical issue, rather it determines how competitors, and thus concentration, are measured. Industries are not markets. Instead, they are defined for the sake of statistical purposes and their classification is based on production processes.

Boeing and the US aircraft industry provide a vivid example. Using industry-level aggregates boils down to assuming that airplanes compete against helicopters and dirigibles. Furthermore, national aggregates fail to put Boeing and Airbus—a European firm—into the same relevant world-wide product market of wide-body aircraft. They also fail to identify the “small jet” market, which throughout the 2010s consisted of a European firm (Airbus), a Canadian firm (Bombardier), and a Brazilian firm (Embraer). Thus, it is clear that, in some cases, industry classifications are broad enough to include not just competitors, but also suppliers, customers, and other firms that do not compete in the same market. Industry classifications may also err on the other side if they do not include all relevant competitors.

“Market power appears to be the most consistent driver of concentration levels and their increasing trends.”

In a recent study, we propose assessing the issue of concentration by using a completely different data source. We base our analysis on a novel dataset constructed by analyzing the merger control decisions of the Directorate-General for Competition (DG Comp) the European Commission. Reports concerning all of its decisions are published online. We read and categorized almost all DG Comp 5,111 merger decisions from 1990 to 2014. These are generally large transactions affecting several EU Member States – like the UK, Germany, France, the Netherlands, Spain, and Italy – if not larger EU-wide or worldwide markets. Since each merger case potentially affects different markets—either in terms of products or in terms of geography—the full dataset contains 30,997 antitrust markets.

For each of these markets, the European Commission performs a careful analysis, first defining the relevant antitrust geographic and product market based on the concept of substitutability, then performing a competitive assessment. Concerning the geographic dimension, 64 percent of relevant markets are defined by DG Comp as national, 25 percent as EU-wide, and 11 percent as worldwide. In a few cases, the geographic market definition is left open. Concerning the product dimension, the Commission identifies the effective competitors acting in the same market for each affected product of the merging parties.

In the majority of these combinations of geographic-product markets, the Commission explicitly reports in its competitive assessment figures on the market shares of the merging firms as well as their major competitors. This allows us to calculate sensible concentration measures as, for instance, a market-specific Herfindahl-Hirschman index (HHI)—i.e., the sum of squared market shares of all firms in a relevant market. Because market shares are not always or fully reported, we can calculate such measures for around two-thirds (over 20,000) product/geographic antitrust markets affected by over 2,000 mergers.

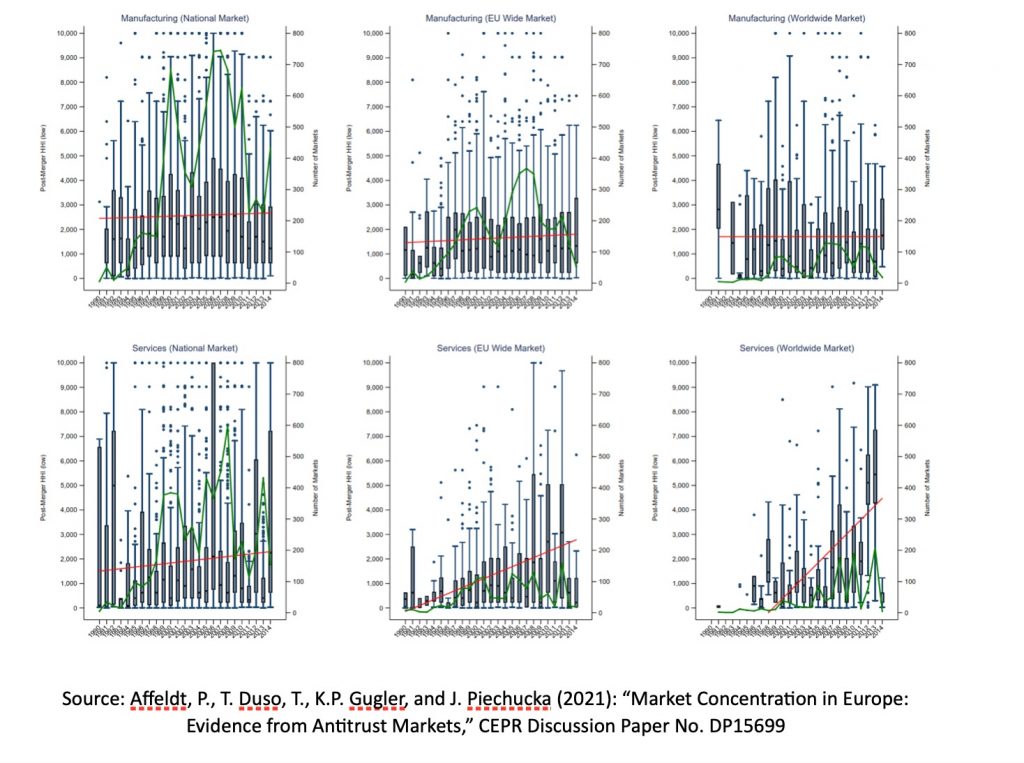

With this data, we show that the concentration measures in these relevant antitrust markets are 3-10 times larger than what the literature otherwise documents. We also confirm that concentration has indeed increased over time, on average. However, we show that there is a great deal of heterogeneity across several dimensions. The extent of the geographic market, as well the broad sector of activity, play a crucial role in this assessment.

Concentration trends in manufacturing are stable at high levels and average concentration is particularly high in narrowly-defined national markets. While starting from a lower level, there is a trend of increasing concentration in the service sectors, regardless of the geographic market considered. Yet, the trend appears to be much steeper in broader EU-wide and worldwide markets. Finally, and perhaps most importantly, we observe some heterogeneity around these trends across and within industries.

But what forces are driving the large heterogeneity in concentration levels between product markets? And are these the same forces that explain the high average level in manufacturing and the different trends across sectors? We identify important elements that correlate with these concentration measures. Barriers to entry are unambiguously positively correlated with concentration, irrespective of time periods, sectors of activity, and geographical market dimension analyzed.

Although strict past merger enforcement negatively correlates with concentration, it appears that this correlation was stronger between 1995 and 2004 than it was in subsequent years. The intangibility of investments displays a consistent positive correlation with concentration only for wider than national—EU wide and worldwide—services markets.

These results might help shed light on the controversial discussion whether concentration reflects the increased market power of dominant firms, or rather the higher efficiency of few super-star firms. Our findings show that possibly both forces are at play, but their relative importance differ. For instance, the fact that concentration correlates with intangible investment points to potentially important efficiency and scalability effects. Yet, these seem to be relevant only in broad EU-wide and worldwide services markets.

Instead, barriers to entry, one of the most formidable sources of market power, appear to matter in all markets—both in manufacturing and services and independently of their geographic extensions—and are economically the most important correlate to concentration. Finally, strict merger control seems to have systematically reduced concentration in the past.

The discussion on how to measure concentration and what economic factors are behind its dynamics has important policy consequences. Our main conclusion is that market power appears to be the most consistent driver of concentration levels and their increasing trends. Thus, strict merger enforcement and, more generally, stricter competition policy that reduces barriers to entry are key tools to keep markets open and competitive. However, tearing down barriers to entry is not the sole task of antitrust authorities. Other policy areas such as regulation, institutions setting norms and standards, and international cooperation agreements must contribute.

This conclusion notwithstanding, there are circumstances in certain antitrust markets in which intangible assets and firm’s scale play a key role where increasing concentration may indeed be likely related to increasing efficiency. It is the task of policymakers to strike the delicate balance between these forces.