Digital marketplaces make comparing credit lending options easier for potential borrowers. However, Jeromee “JJ” Johnson cautions that online platforms may be turning comparison itself into a signal to lenders—at a cost to applicants.

Digital credit marketplaces like LendingTree and Credible are meant to offer a faster and easier lending option for potential borrowers. Online platforms give borrowers access to multiple potential lenders so they can compare offers such as annual percentage rates (APR), total costs, and fees. By making lenders compete, borrowers increase their chances of getting a better loan. However, online credit marketplaces have access to data that one’s local bank does not, such as search and transaction history and number of applications. This additional data influences the numbers that lenders offer borrowers, costing them thousands of dollars. In online credit markets, credit is not the only criterion that matters. The act of shopping for a loan itself can change the price of credit.

What happens when you shop for a loan

Shopping is essential to finding a loan. The Consumer Financial Protection Bureau tells homebuyers that getting loan estimates from multiple lenders can save them $600 to $1,200 a year. The advice is sound. A few basis points, a fee, or a timing difference can compound over decades.

The evidence from America’s mortgage market shows why. In a Philadelphia Federal Reserve working paper, Neil Bhutta, Andreas Fuster and Aurel Hizmo found that half of American mortgage borrowers seriously considered only one lender. Just 3% considered more than three. Yet 95% said they were satisfied that they had received the lowest rate for which they could qualify.

Many had not. Traditionally, lenders will offer approved borrowers a lender credit, which limits upfront costs in exchange for a higher interest rate. In this study, the authors found that someone taking out a $250,000 mortgage loan in the 90th percentile, paying among the highest interest rates in the market, should have been receiving $6,250 more in lender credits to cover upfront costs compared with someone in the 10th percentile. However, these credits were often missing for the least financially sophisticated borrowers, such as those who failed to shop for multiple offers.

Despite the financial costs of not shopping for loans, research is showing that shopping may come with its own side effects.

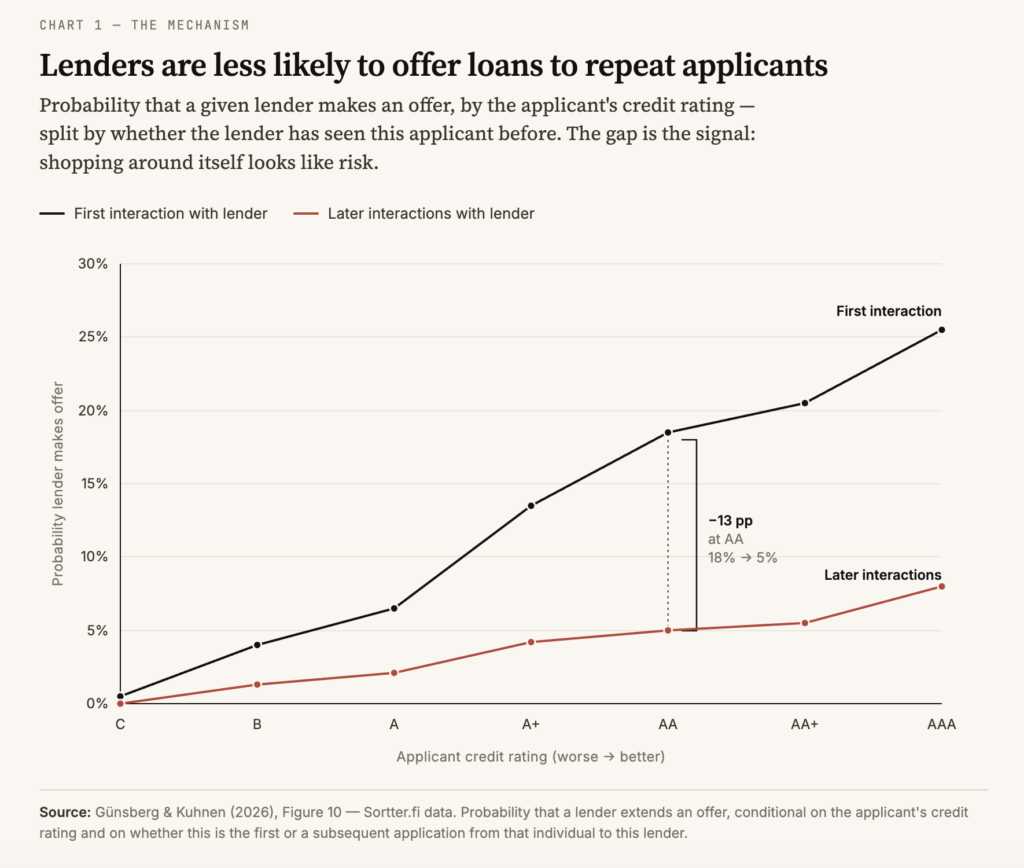

An NBER working paper by Alex Günsberg and Camelia Kuhnen gives the cleanest evidence so far. The authors studied Sortter.fi, Finland’s largest online loan marketplace. Their data covered 736,802 applications, 747,855 offers, and 208,932 people from 2019 to mid-2024. On Sortter.fi, an applicant submits one form with their personal information and desired loan terms and receives algorithmic offers within minutes from the 15 to 20 lenders active on the platform that day. Applicants can apply again, change requested terms, and reject offers. During the sample period, repeat applications had no effect on Finland’s national credit registry. The formal credit score penalty was not the problem.

The paper found that search is valuable for borrowers. The identity of the lender itself (lender fixed effect) has a modest impact on loan size and maturity and a high effect on offered APR. Borrowers therefore have reason to search across time, lenders, and loan terms. In this study, borrowers used the market actively. The mean number of applications per person was 3.56. The median was two. Among applications that received at least one offer, the applicant selected no offer 47% of the time. The marketplace was being used as designed.

But it created a new design problem. Lenders penalized repeat applicants. For an applicant with a high credit score, the chance that a given lender made an offer fell from 18% in a first interaction to 5% in a later one. Conditional on making an offer, the APR including fees was 0.7 percentage points higher when the lender had seen the applicant before.

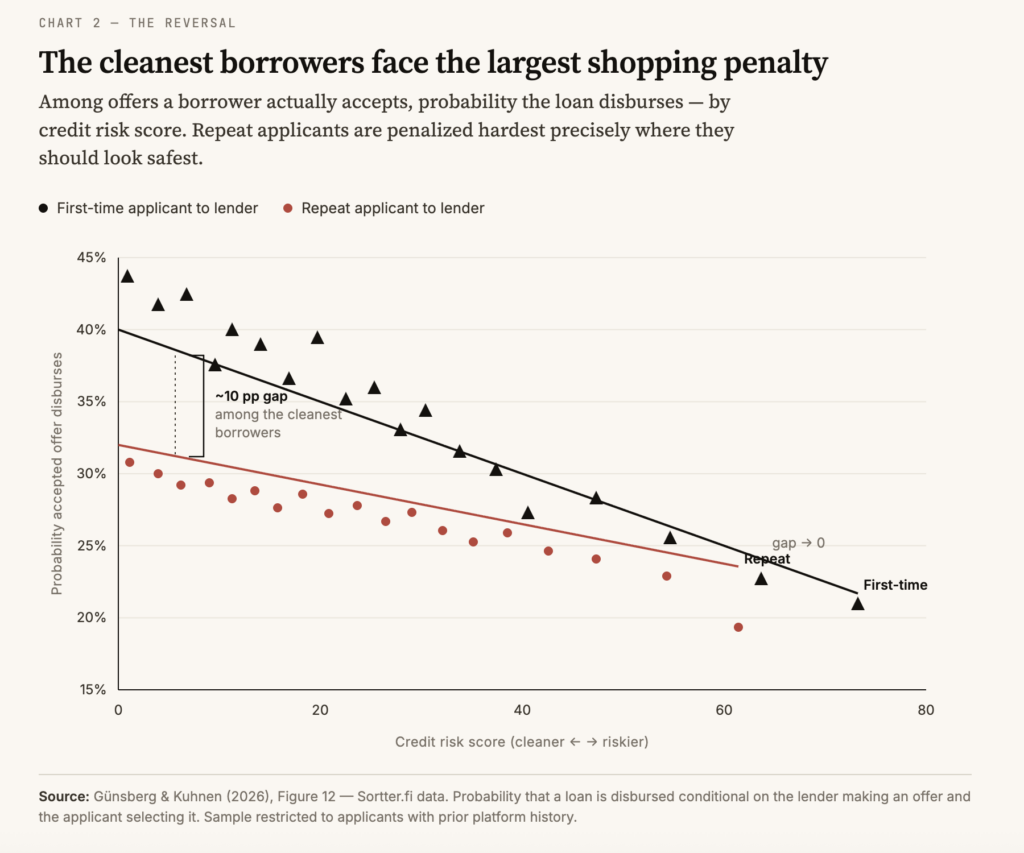

The evidence on disbursement, when the lender sends the funds, is even sharper. Because the lender mix on platforms changes daily, a borrower might look like a first-time applicant to some lenders and a repeat applicant to others. For the lowest-risk borrowers, a lender seeing them for the second time is 10 percentage points less likely to disburse the loan than a lender seeing them for the first time. Even if the loan does close, these ‘clean’ shoppers face a pricing penalty: lenders charge repeat applicants an average of 0.7 percentage points more in APR and fees. The very borrowers the market should treat as safest face the largest penalty for simply trying to find a better deal.

Why is search being penalized?

The problem for borrowers using online credit marketplaces is that two categories of information are being collapsed. Credit-risk information concerns a borrower’s ability and willingness to repay based on income, debt, collateral, delinquencies, loan-to-value, debt-to-income, and repayment history. In the United States and Finland, much of this is encapsulated within a user’s credit score. Borrower-permissioned cash-flow data can extend that picture.

Search information is different. It describes how the borrower moved through the market: how often they searched, the timing of their return visits to the platform, whether they changed requested terms, which offers they rejected, and which prior interactions did not convert into loans.

The two categories can be correlated, because intensive search behavior often signals unobserved risk or financial urgency that a static credit score cannot yet capture. Lenders use this ‘search-path’ data to detect if a borrower is being rejected elsewhere or to identify the highest interest rate a borrower is desperate enough to accept. Credit-risk data answers whether a borrower is likely to repay. Search data often answers another question: what did the borrower reveal while trying to get a better deal?

It’s all in the design

This is a classic platform-design problem. Platforms choose what sellers see, when they see it, and how disclosure affects price competition. Jacopo Gambato and Martin Peitz make the point that platforms, sellers, and consumers often have diverging incentives over whether or not to disclose consumer information, and how much to leave up to consumer discretion. Lending marketplaces should be understood that way: online platforms are not neutral—they decide how disclosure is structured, and these disclosures influence pricing.

The answer cannot be to offer lenders “less data.” Credit markets need information. However, the obverse that we should offer lenders “more data” doesn’t hold, either. Mark Jansen, Fabian Nagel, Constantine Yannelis, and Anthony Lee Zhang show that giving lenders more data can allow prices to align more closely with borrowers’ costs. In economic theory, this raises total welfare, but it does so while shifting surplus from borrowers to lenders. More information can make pricing more efficient and still leave borrowers worse off.

What information lenders receive changes the terms for borrowers. Tailoring information to raise borrowers’ surplus does not have to be zero sum. Sebastian Doerr, Leonardo Gambacorta, Luigi Guiso, and Marina Sanchez del Villar find that after California’s Consumer Privacy Act (2020), fintech mortgage market share increased, fintech lenders used more nontraditional scoring, and fintech loan rates and default rates declined relative to other lenders. By leveraging borrower-permissioned cash-flow data, these lenders were able to move toward more precise, individualized risk profiles that rewarded creditworthy applicants. This governance-led transparency allowed fintechs to lower interest rates for consumers while simultaneously reducing default rates, demonstrating that clear privacy rules can turn data into a shared benefit rather than a penalty. Better data can improve screening. Better governance decides which data should be used, by whom, and for what.

Electronic trading has navigated versions of this problem for decades. At the private trading company I co-founded, 3D Markets, we saw what happened when a large trade was revealed too early: it essentially tipped the trader’s hand. By showing the market exactly what they wanted to buy (or sell) and how quickly they needed it, the trader ‘signaled’ their strategy to everyone else. Other parties, seeing this urgency, could then react by adjusting their prices, making the trade much more expensive for the person who was just trying to find a buyer. Changing venue design was the response. It decides who can see what, when, and under what conditions. Too much transparency at the wrong time creates price impact. Too little creates unfairness or low confidence. The task is to reveal enough information to support execution, but not so much that seeking liquidity becomes the trader’s penalty.

Regulators have already targeted the most obvious ways that a person’s intent to borrow money is exposed to others. A primary example is the Homebuyers Privacy Protection Act (2025), which restricts credit bureaus from selling ‘trigger leads’—a practice where other lenders are notified the moment you apply for a mortgage. While these leads are a ‘loud’ problem because they result in constant sales calls, the search data collected by online marketplaces is ‘quieter’ and harder to spot. Even so, the fundamental question remains the same: who is watching your search behavior, and how are they using that knowledge to change the terms you’re offered?

Credit scoring addresses part of the problem. The Consumer Financial Protection Bureau’s (CFPB) guidance says multiple inquiries for the same loan type within a short window are generally treated as one inquiry for scoring. But score protection is not information protection. Recent inquiries remain visible in mortgage underwriting. Fannie Mae’s Selling Guide tells lenders to review their number and recency because they may show that a borrower has been actively seeking new credit.

The CFPB has also addressed a more visible platform failure: comparison tools and lead generators that steer consumers based on operator compensation rather than consumer interest. Its 2024 circular focuses on preferencing and steering. Search-path leakage is a subtler market-design problem. Even honest rankings can fail borrowers if comparison itself becomes adverse pricing information.

Redesigning loan markets to protect borrowers

Search data should be treated as separate from credit-risk data. If repeat-applicant status, rejected-offer history, or prior search behavior is not needed to underwrite the file, prevent fraud, or comply with law, lenders should not see it. Marketplaces should disclose when search behavior may affect the terms borrowers see. A borrower cannot make an informed choice about how often to search if the marketplace presents search as free while treating it as costly.

Marketplaces must test and monitor outcomes. Do repeat shoppers receive fewer offers or worse terms after controlling for credit characteristics, loan terms, timing, and lender mix? Do high-quality borrowers experience worse disbursement after prior comparison? These are measurable questions. Not asking them is itself a design choice.

Borrowers are doing what the market tells them to do. Lenders are doing what markets train them to do. The marketplace is where the design responsibility sits.

A comparison marketplace should not punish comparison.

Author Disclosure: The author is President of Tellus App, Inc., a real estate and financial technology company. Tellus does not operate a lending marketplace, does not make consumer loans, and has no affiliation with the papers, platforms, lenders, or marketplaces discussed. The author has no current connection to 3D Markets. The author received no compensation or support from any party discussed in this article. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.