In recent years, ESG reports have become more common for publicly traded companies. However, critics have found the information they provide to be inconsistent and thus their utility for inter-firm comparisons uneven. In new research, Ethan Rouen, Kunal Sachdeva, and Aaron Yoon argue that the past introduction of voluntary standards for ESG reporting has led firms to produce a more focused disclosure, suggesting that new standards and mandatory disclosure policies has the potential to help investors understand firms’ exposure to ESG risks, including climate change.

ESG (Environmental, Social, and Governance) reports have been gaining traction in recent years as more and more companies are realizing the importance of being transparent about their actions and progress in these areas. At the start of the twenty-first century, only a handful of companies released information about their ESG activities. However, as of 2021, most large publicly traded companies, both in the United States and worldwide, have begun publishing separate ESG reports. Despite this increase in ESG reporting, research on the information contained in these reports is limited due to the lack of a centralized database for ESG reports and the fact that these reports are not standardized in terms of content and format, making it difficult to compare information from different companies and industries.

To address these challenges, regulators are exploring the possibility of implementing reporting mandates to establish a standardized framework for disclosing ESG activities. Such mandates would likely improve the transparency and comparability of ESG reporting, making it easier to compare information from different companies and industries. However, there are some concerns that mandating ESG information could impose additional costs on companies, as seen in recent debates around the US Securities and Exchange Commission’s proposed rule requiring companies to disclose their direct and indirect greenhouse gas emissions to help investors understand their exposure to climate-change risk. Given this, it is crucial to conduct careful empirical analyses to evaluate the potential impact of introducing ESG-related standards and disclosure mandates.

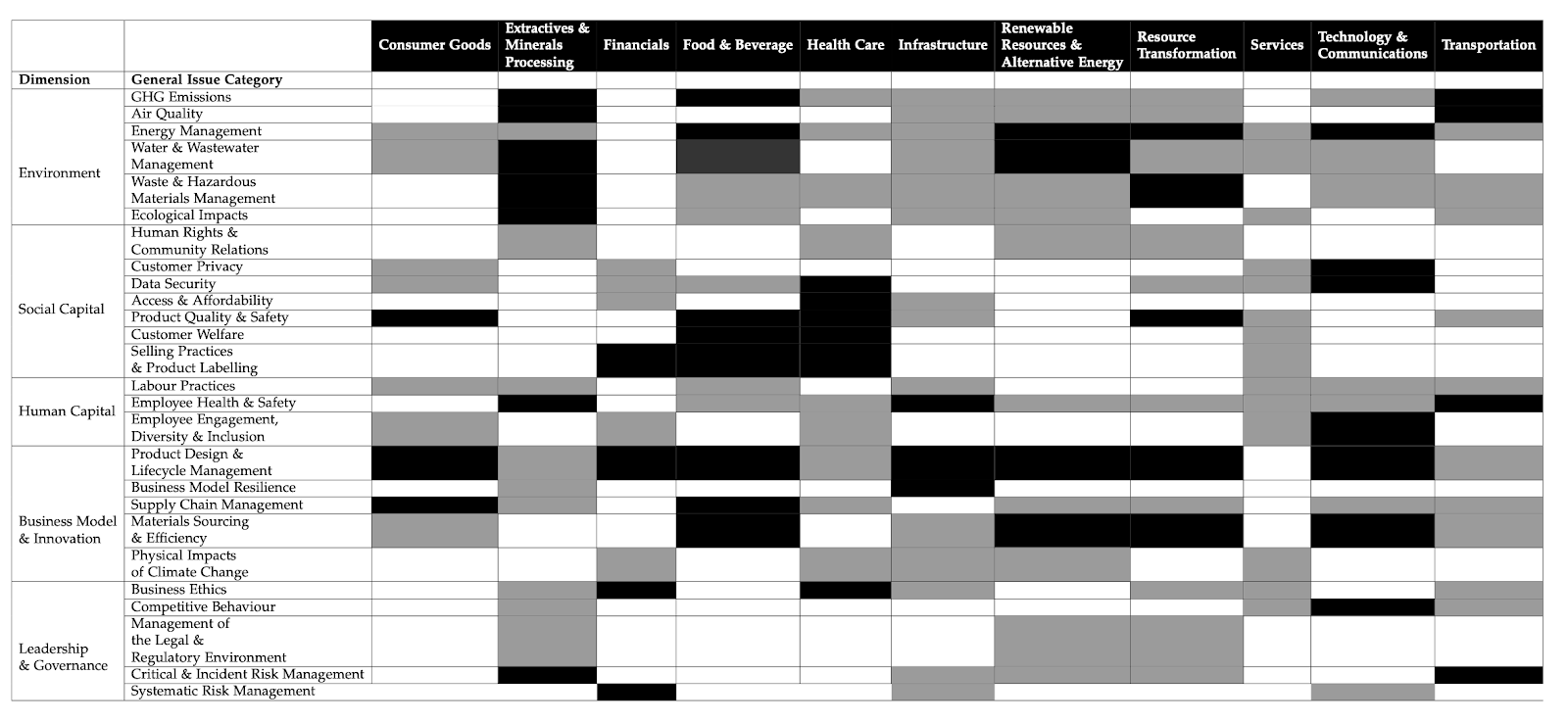

In a working paper, we examine ESG reports to gain new insights into their evolution and the impact of voluntary standards on the information disclosed by companies. We manually collected ESG reports from S&P 500 firms between 2010 and 2021 and analyzed their content and evolution over time using machine learning techniques. As an analytical framework for categorizing the content companies expressed concern about, we used the SASB (Sustainability Accounting Standards Board) provisional standards. The SASB identifies 26 key dimensions of ESG issues and classified those issues as financially material or not, according to the industry that companies operate in.

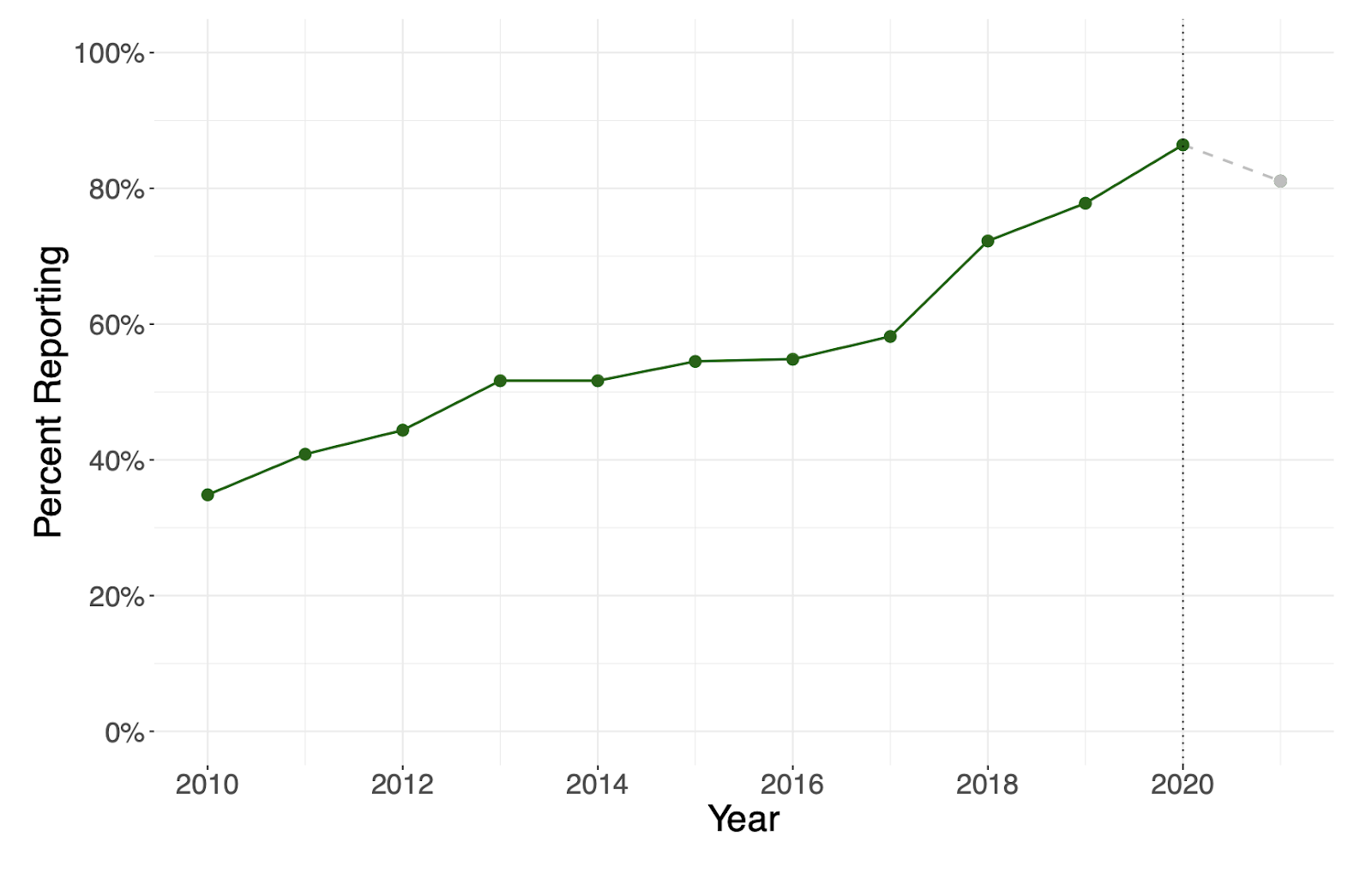

Our data illustrates a rapid growth in firms releasing ESG reports, with the proportion of firms releasing ESG reports increasing from 35% in 2010 to 86% in 2020. However, we also noted a slight decrease in 2021, as a group of companies that published reports in 2020 had not yet done so for 2021 at the time the data was collected.

Figure 1: By analyzing data from S&P 500 firms between 2010 and 2021, we found that the proportion of firms releasing ESG reports has increased dramatically, from 35% in 2010 to 86% in 2020. However, it’s worth noting that there was a slight decrease in 2021, as some companies that published reports in 2020 had not yet done so for 2021 at the time the data was collected.

Figure 2: To provide a framework for our analysis, we used the SASB (Sustainability Accounting Standards Board) provisional standards. SASB identified 26 key ESG-related topics across five dimensions. SASB determined which topics are material for each of 11 sectors, recognizing that the financial relevance of topics can vary significantly between sectors.

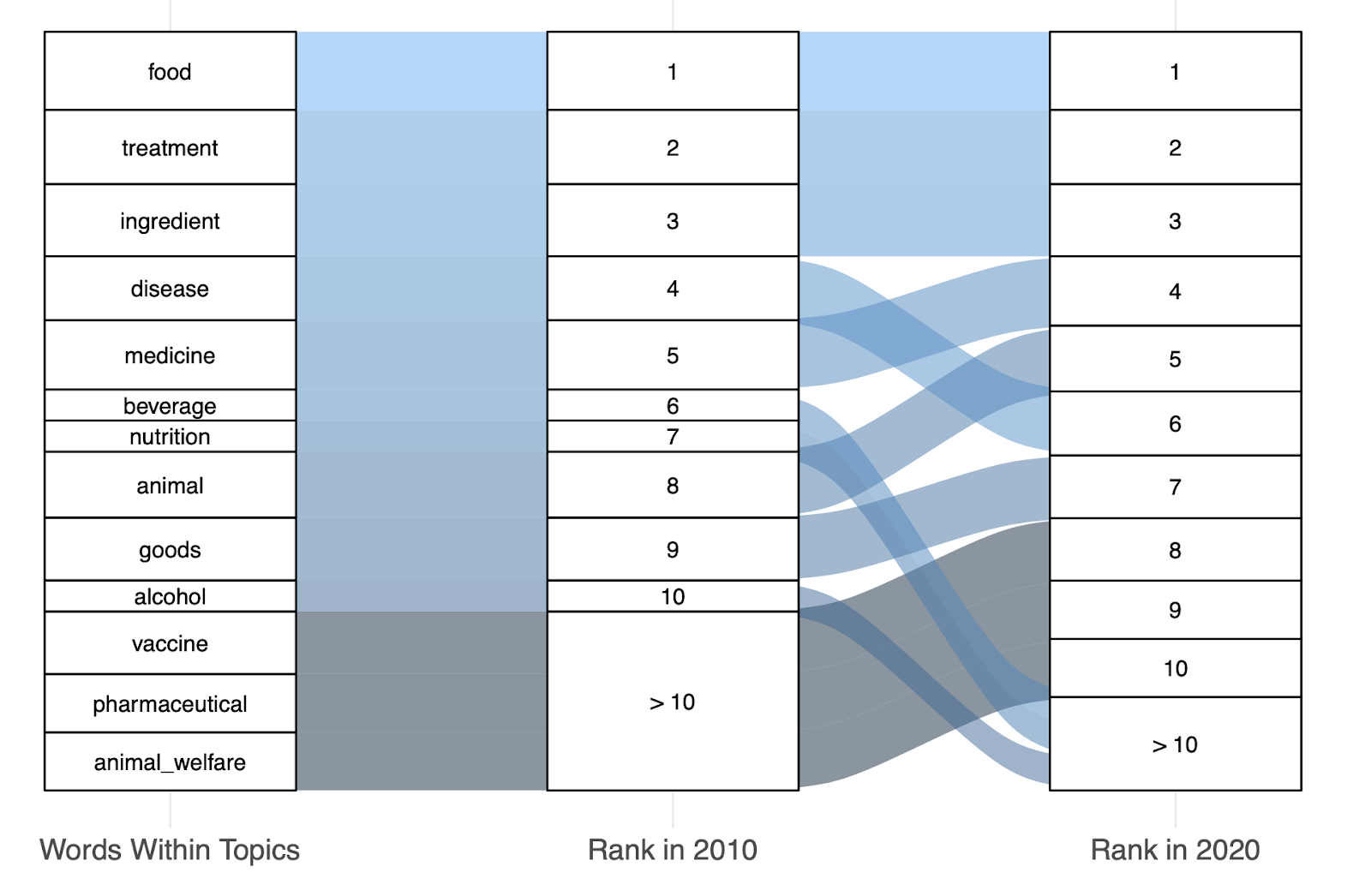

We conducted our analyses at three levels. Our first level of analysis examined how the language used to discuss specific ESG topics has evolved over time. By using advanced machine learning techniques, we were able to uncover trends in the way companies discuss various ESG topics. For example, we found that terms related to customer welfare, such as “vaccine,” were not frequently used in ESG reports in 2010, but have become increasingly prevalent in 2020, likely due to the impact of the Covid-19 pandemic.

Figure 3. The chart shows how the frequency of key words identifying specific ESG topics have evolved over time, conveying which topics have increased and decreased in terms of importance for ESG reporting.

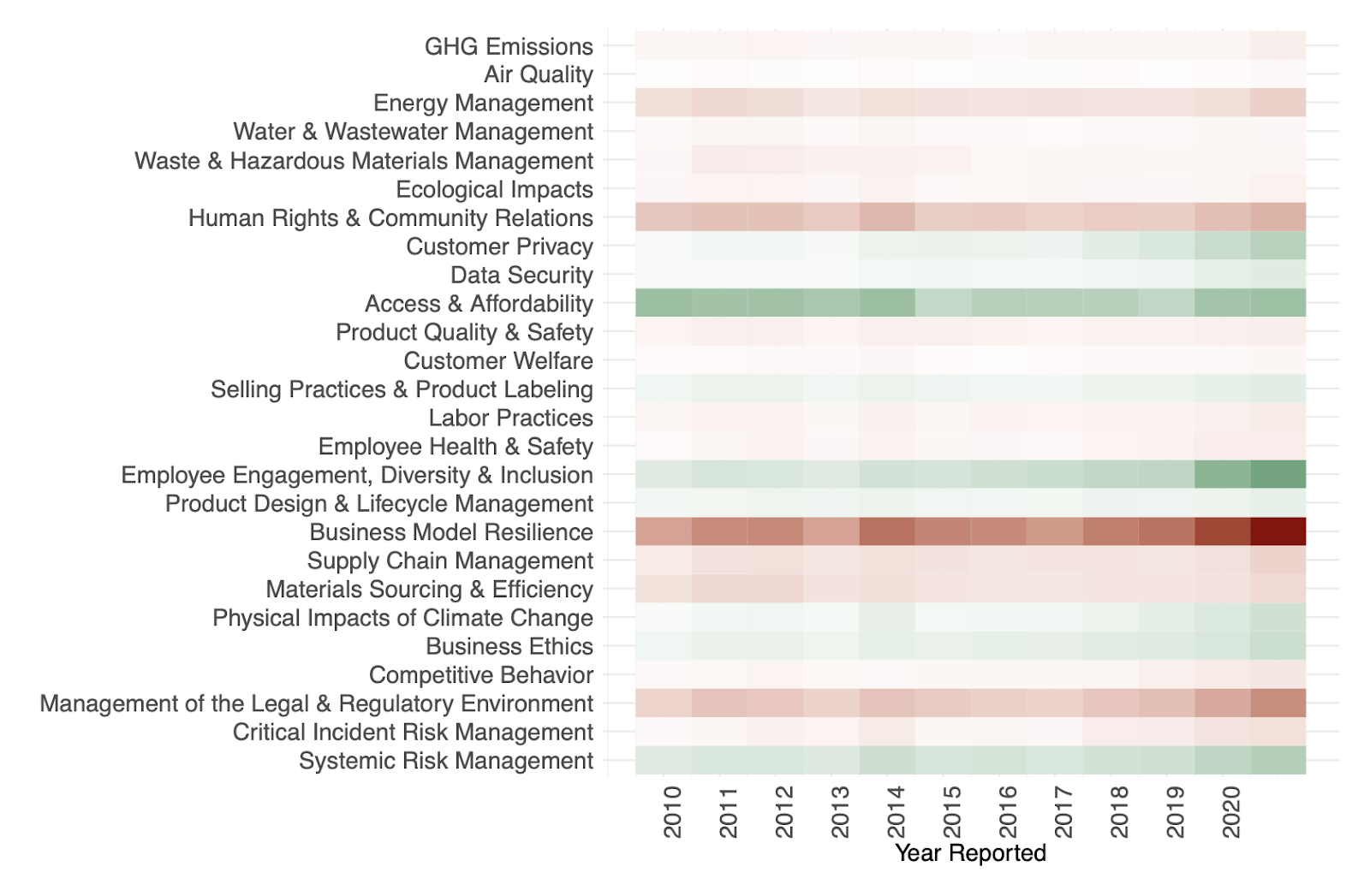

Our second level of analysis introduced new measures that allow us to study the evolution of firms’ emphasis on different ESG topics at the sector level. By using heat maps, we compared the amount of information provided by firms in the financial sector for each topic in each year of our sample. The heat maps use green and red bars to indicate whether a topic is considered material or immaterial for the sector and the darkness of the shading represents the average amount of information provided by firms for that topic.

Figure 4. The chart displays how financial firms have emphasized or deemphasized certain ESG topics over the last decade. Green bars indicate that a topic is material for the sector and red indicates that it is immaterial. The darker the color’s shading, the more information firms have provided on that topic on average.

Our findings highlight the importance of understanding the evolving priorities of firms and how they align with regulatory standards. On average, firms devote most of their reports to topics that are material to their sector, disclosing 48% more information on material topics relative to immaterial topics. Additionally, we used the staggered introduction of SASB’s voluntary guidance on material ESG issues to study if and how firms changed their disclosures after the release of the guidance. Our results show that the relative amount of material information increased by 11% after the release of voluntary standards.

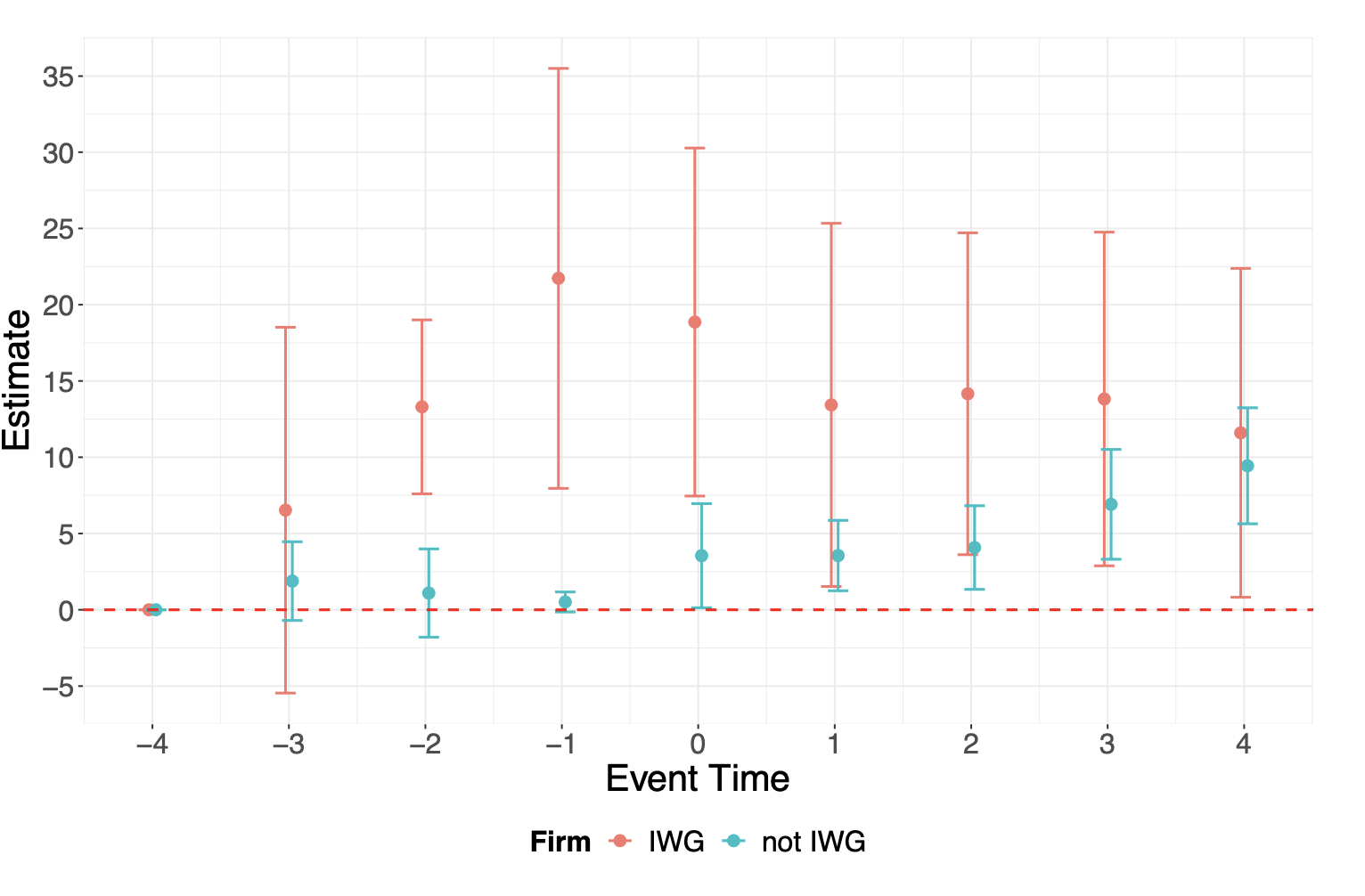

We also explored the role of SASB guidance and examine which firms follow the voluntary guidance. Our analysis shows that firms that participated in developing the SASB standards (i.e., members of Industry Working Groups (IWGs)) appeared to learn while doing, gradually increasing their material disclosures as the standards were created. Other firms appeared to respond to the release of the standards and increased their material disclosures at a slower pace over a similar period.

Figure 5. Companies that were part of the Industry Working Groups that developed the SASB standards were much faster in adopting material disclosures. The x axis shows the time in years from the publication of the SASB standards.

These findings provide evidence that standards, even voluntary ones, can serve as powerful guidance when a large sample of firms chooses voluntary disclosure in the absence of regulation. They also suggest that disclosure leaders (i.e., IWG firms) can learn while doing, while other firms may be equally quick to adapt once standards are released.

Overall, our research provides a portrait of the relation between standard-setting and firms’ ESG disclosures. On average, firms gravitated toward material disclosures once materiality was defined, but this response was not uniform across firms. Our findings indicate that having well-defined voluntary standards and guidance can enhance the quality of ESG disclosures, making it easier for investors to compare and evaluate companies. This is particularly relevant as regulators are currently considering imposing ESG disclosure mandates, such as the ESG Disclosure Simplification Act of 2021 proposed by the U.S. Congress. Our research suggests that a mandate would likely lead to greater convergence in the types of information reported by companies, which could make it easier for investors to make informed decisions.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.