In new research, Ben Bates examines the recent wave of funds designed to open private markets to retail investors. Such funds both underreport volatility and perform worse than comparable funds aimed at wealthier investors.

For decades, investing in the United States has been divided into two markets: a public market and a private market. The public market is open to everyone, and the private market is accessible only to investors deemed sufficiently wealthy or financially sophisticated. A popular story has been that the U.S.’s two-tier market puts the wealthy and the masses on starkly different wealth-building trajectories. While middle-class Americans patiently save by buying public stocks and bonds, the wealthy seem to be amassing untold riches through their exclusive investments in private funds and hot tech startups.

Recently, the landscape has begun shifting rapidly. Asset management firms are launching a slew of new investment products that open private markets to “retail” investors. Furthermore, the Trump administration has made it a policy priority to get private investments with reputably higher returns into working Americans’ retirement accounts.

While “democratizing” private markets creates new opportunities for retail investors, these opportunities come with new risks. Private market practices have developed without significant regulatory oversight, and the markets themselves have long been dominated by sophisticated players, potentially leaving inexperienced investors vulnerable.

My recent work, “Retail Access to Private Markets,” analyzes the first major wave of retail-focused, private credit investment vehicles, which I call “retail private funds.” I highlight two hazards that these funds pose to retail investors. First, the funds’ reported returns may substantially understate their risk. Second, the funds made available to the broadest groups of investors seem to perform worse, on average, than funds sold exclusively to wealthier customers.

Underreported risk

From 2015 to 2024, retail private funds structured as business development companies (BDCs)—the most common type—reported average annualized returns of 7.6% per year with remarkably little variation from quarter to quarter. These reported returns are based on dividends paid by the BDCs and changes in the estimated net asset values (NAVs) of the BDCs’ portfolios. Sharpe Ratios are commonly used in the asset management industry to summarize risk-adjusted returns, and during this period, BDCs’ reported returns had a remarkable average Sharpe Ratio of 1.12. In comparison, the Sharpe Ratio of the public stock market as a whole was only 0.65.

Unfortunately, two pieces of evidence suggest that BDCs’ reported performance may be too good to be true. First, a subset of BDCs (called “public BDCs”) like Blackstone Secured Lending Fund and Ares Capital Corp. have shares that trade on public exchanges, so it is possible to calculate their returns based on changes in their share prices rather than their estimated NAVs. The average volatility of these public BDCs’ market price-based returns turns out to be 4.3 times higher than the average volatility of their reported, or NAV-based, returns. While gaps between the volatility of market price- and NAV-based returns are normal for traded closed-end funds, the magnitude of the gap for public BDCs is so large that it raises suspicion.

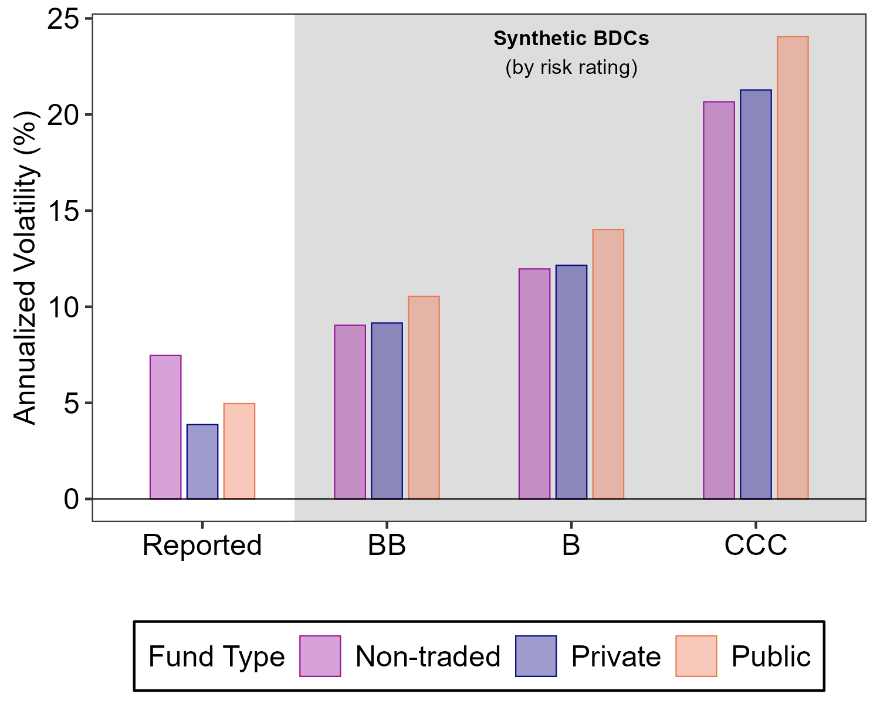

Second, BDCs’ average reported volatility seems implausibly low when compared to the volatilities of comparable, publicly traded investments. In Figure 1 below, I compare the average reported volatilities of the three BDC types (“public,” “private,” and “non-traded”) with the volatilities of “synthetic” BDCs. I construct the synthetic BDCs’ returns by combining the returns of several leveraged loan indexes of varying credit risk levels with BDC-like leverage and fees. The synthetic BDCs allow me to approximate what BDCs’ volatilities would be if their underlying investment returns fluctuated in lockstep with public markets. I use leveraged loans as the asset base because they, like BDCs’ private credit loans, are generally high-yield, floating-rate loans to middle-market companies. The synthetic BDCs have volatilities ranging from 1.2 to 5.5 times higher than the actual BDCs’ reported volatilities.

Figure 1: Annualized Volatility of BDCs and Synthetic BDCs by Type

BDCs’ underreported volatility creates three distinct ways for retail investors to get into trouble:

1. Investors with low risk tolerances might put too much money into BDCs or similar products.

2. Unlike traditional private funds, which typically lock up investors’ capital for years, most retail private funds offer periodic liquidity. If retail investors ask for their money back en masse during a downturn, their fund managers will have to either sell assets at a loss (relative to their reported valuations) to fund investors’ redemption requests or refuse to honor the requests altogether.

3. If fund managers do allow some investors to cash out at inflated valuations during a downturn, they transfer value from the “stayers” to the “leavers,” and the stayers are stuck bearing a disproportionate share of their funds’ losses.

Retail investors get the worst products

The bulk of the BDC market today is made up of funds that do not have exchange-traded shares. The two types of nonpublic BDCs—private BDCs and non-traded BDCs—make similar investments, use similar amounts of leverage, and both offer investors only periodic liquidity. However, they are sold to different classes of investors. Generally speaking, anyone with more than about $70,000 in annual income and more than $70,000 in savings can invest in non-traded BDCs. But to invest in private BDCs, an individual must have $200,000 in annual income or a net worth of over $1 million.

I compare the quarterly net returns of non-traded and private BDCs, controlling for fund size, fund leverage, and underlying investment type. I find that private BDCs’ returns are, on average, about 0.6 percentage points higher each quarter than non-traded BDCs’ returns. Over the course of a year, this adds up to a roughly 2.4 percentage point difference in net returns.

These results are consistent with a theory where less wealthy and less sophisticated investors are offered worse products than wealthier and more sophisticated individuals and institutions. Alternative explanations consistent with the data exist and cannot immediately be ruled out, including that non-traded BDCs hold more cash to manage their liquidity or that their loans have lower default risk. Nevertheless, the possibility that retail investors face adverse selection in private markets should be taken seriously given the magnitude of the return gap between the two products.

Policy

Retail private funds are here to stay, so what can policymakers do to mitigate the problems they create? In the paper, I discuss the pros and cons of a variety of policy options in detail, four of which I’ll highlight here:

1. Push for more market-linked valuations. The federal securities laws and accounting standards already require BDCs and similar fund products to value their investments at “fair value,” or the price at which those investments could be sold in a market transaction. But even though the data suggest that BDCs underreport volatility, proving a fraud case against a particular manager would be difficult, if not impossible. The Securities and Exchange Commission may be able to do more with its informal tools to signal that it has concerns with current valuation practices and would like to see changes. For example, the SEC could rigorously scrutinize private credit valuation practices through its examination program or issue informal guidance on the subject.

2. Require additional disclosure about valuation methods. The SEC could ask funds to publicly disclose (1) the modeling assumptions they use for each of their investments, (2) contemporaneous price changes for comparable traded assets, or even (3) formal valuation opinions from third-party valuation consultants (which many advisers already employ). These types of reforms would increase transparency and subject valuation practices to greater market discipline, but they would be much costlier than informal tools.

3. Reduce incentives for product sorting. The SEC could institute regulatory reforms that make it more attractive for fund managers to add retail investors to products they would otherwise sell only to wealthier investors. The SEC should accompany any such reforms with vigilant oversight of the brokers and investment advisers who sell these products to retail customers. Even with these changes, individuals may still have to pay higher fees than institutions to access the same funds. However, fee-based price differences are much more transparent to retail investors than product-based sorting and are therefore, in my view, normatively preferable.

4. Allow retail private funds only within employer-sponsored retirement plans. In theory, this proposal could increase the quality of fund options available to retail investors because their employers (1) may be able to gain access to better funds by offering a larger pool of capital and (2) could hire professionals with the skills to screen the quality of potential funds. Employer-sponsored retirement plans are also subject to the Employee Retirement Income Security Act (ERISA), which is meant to ensure that employers act in their employees’ best interests when selecting fund options. As a bonus, confining retail private funds to retirement accounts might reduce retail investors’ incentives to trade in and out of the funds, mitigating the problems caused by their semiliquid structures and questionable valuations.

The retirement plan-based approach comes with several significant dangers, however. Primarily, it puts lots of pressure on ERISA and employers’ human resources departments to make sure retail investors get good options. But if ERISA and its enforcement apparatus do not do much to constrain employers’ behavior, then the retirement solution could make things worse than the status quo. Low-quality fund managers would gain an opportunity to influence HR departments into accepting their funds, which would then be filled with the retirement savings of employees who likely would have invested in sensible public market alternatives otherwise.

Authors’ Disclosures: The authors report no conflicts of interest. You can read our disclosure policy here.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.

Subscribe here for ProMarket’s weekly newsletter, Special Interest, to stay up to date on ProMarket’s coverage of the political economy and other content from the Stigler Center.