Some progressive politicians and advocates have argued that lax antitrust policies enabled the inflation surge that began in 2021 and that aggressive antitrust enforcement is crucial to combatting inflation. These assertions are misguided and misleading. Similar greedflation theories emerged during previous inflation spikes, but their promotion this time has proven counterproductive. The allure of trustbusting ideas, it seems, is starting to wane.

In 2021-2022, the Biden administration and progressive allies postulated that permissive antitrust enforcement policies drove, contributed to, or enabled the inflation surge that followed the COVID-19 pandemic. Promoters of these “greedflation” theories contended that sharp rises in living costs were occurring simultaneous to large increases in profit margins throughout the economy because powerful companies were illegally abusing their market power to price gouge consumers. Alternatively, they argued, systemic exploitation of monopoly power had compromised the resilience of supply chains in the economy. While similar populist theories had occasionally gained traction in the 20th century, this time the idea met with criticism and derision. This setback, coupled with other defeats, may signal the beginning of the decline of the Neo-Brandeisian movement.

Present Greedflation

The inflation spike of the 1970s inspired portmanteaus blending trending factors with “inflation,” such as stagflation, kidflation, gradeflation, and taxflation. The inflation surge that followed the Covid-19 pandemic popularized a new one: greedflation.

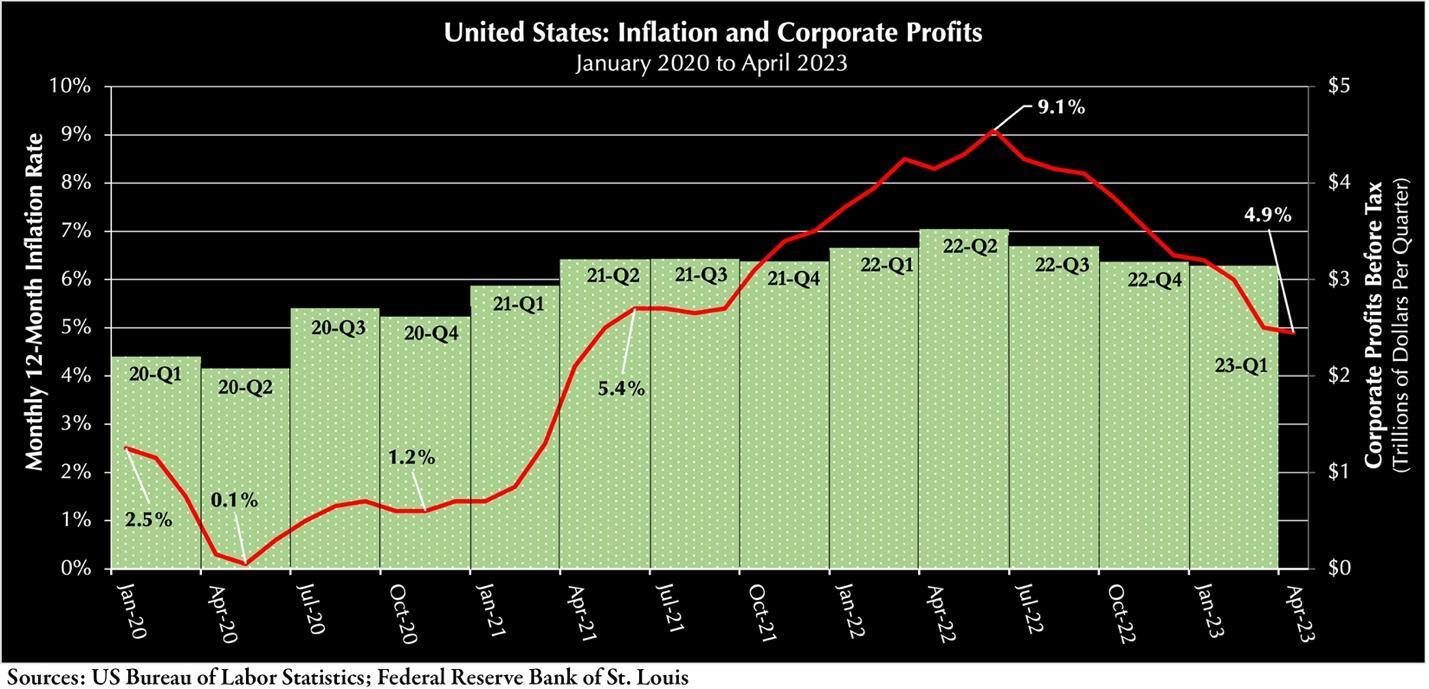

The pandemic triggered a brief dip in prices, with prices hitting lows in May 2020. Prices then began a steep ascent, peaking in June 2022. Corporate profits rose along with inflation, popularizing greedflation theories. Corporate executives were “seizing a once in a generation opportunity to raise prices to match and in some cases outpace their own higher expenses, after decades of grinding down costs and prices,” The Wall Street Journal reported.

The rising number of reports on greedflation provided fuel to critics of big business. President Joe Biden, Senator Bernie Sanders, and Federal Trade Commissioner Chair Lina Khan all accused companies of using their market positions to price gouge consumers. Senator Elizabeth Warren, for instance, argued that “[t]he nation is dealing with inflation at its highest level in decades, much of it driven by corporate greed and anticompetitive behavior,” and that “[a]ntitrust policy plays a vital role in protecting consumers from anticompetitive practices that lead to higher prices.”

The White House took advantage of inflation to pursue its Neo-Brandeisian antitrust agenda but quickly found that its arguments for stricter antitrust as an antidote to inflation were irreconcilable with economic realities. The White House Council of Economic Advisers reportedly objected to theories tying inflation to corporate power and then Director of the National Economic Council Brian Reese likewise tried to soften the White House’s position that antitrust could reduce inflation.

The 2023 President’s annual economic report similarly distanced the White House from assertions that unchecked economic power was the culprit for soaring inflation. The report recognized that some argued that “increased market concentration in U.S. industries” had contributed to the spike in inflation, and that “[t]here is some evidence that these firms [raised] prices in response to cost increases more than firms without market power would have done in the past.” However, the report also stated that “the link between market power and pricing when subject to shocks like the pandemic is not clear. . . . Measuring market power is a difficult task, and measuring the prices firms charge above the cost of their inputs, their ‘markup,’ isolated from the effects of the increased demand and constrained supply of 2022, is even more fraught.”

Misleading Political Memes

The central tenet of competition laws is that, in the presence of barriers to entry, market power tends to result in supracompetitive prices. Among other things, this premise implies that material changes in market concentration may affect prices in the relevant markets.

Inflation represents the rate at which the average prices of goods and services, typically measured by the Consumer Price Index, are changing over time. Inflation does not reflect actual price levels. Accordingly, low inflation indicates a relatively slow rate of price changes, rather than intrinsically low prices. Correspondingly, supracompetitive prices of certain products and services resulting from excessive market concentration are not indicative of high inflation rates.

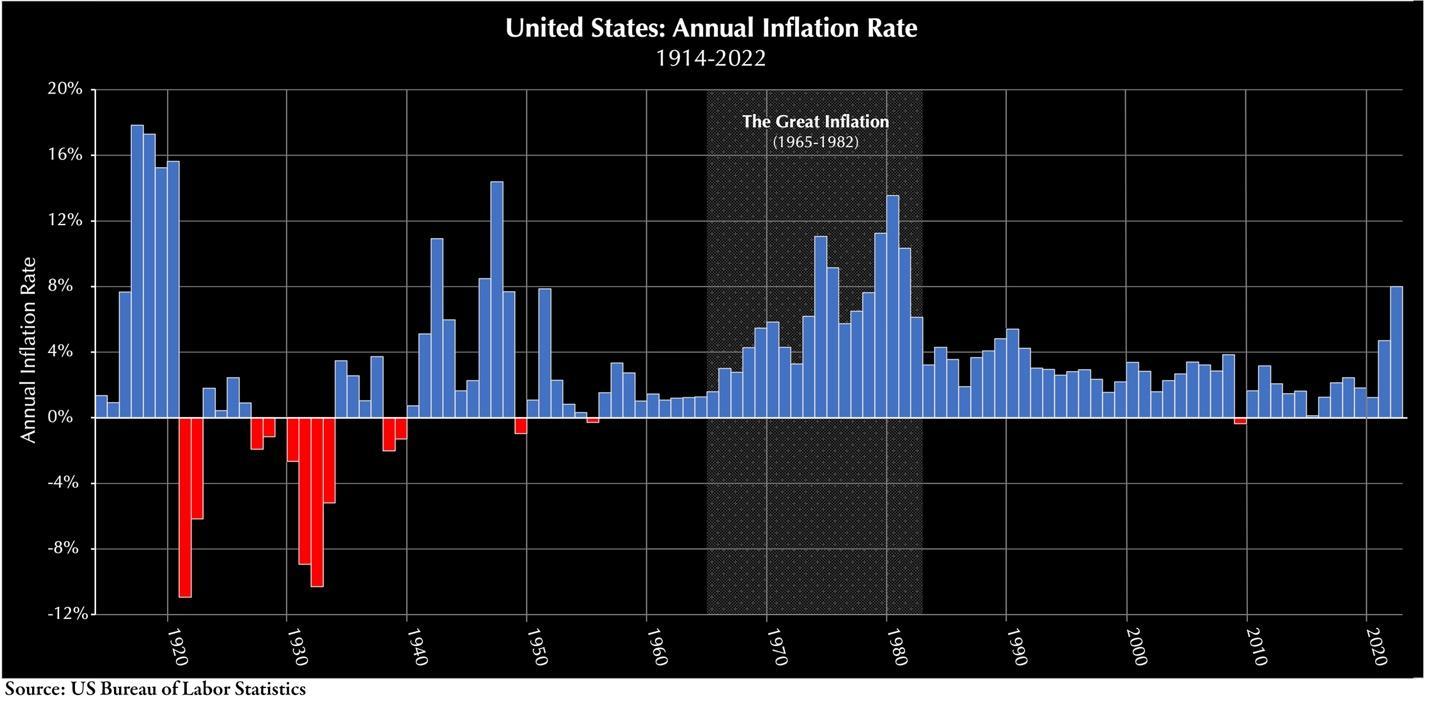

The United States saw high inflation in the eras that contemporary antitrust crusaders describe as antitrust’s golden age. In contrast, for several decades until the onset of the COVID-19 pandemic, the U.S. experienced a period of relatively low inflation, although many industries became considerably more concentrated during that period. As stated in Biden’s 2021 executive order Promoting Competition in the American Economy:

[O]ver the last several decades, as industries have consolidated, competition has weakened in too many markets, denying Americans the benefits of an open economy and widening racial, income, and wealth inequality. Federal Government inaction has contributed to these problems, with workers, farmers, small businesses, and consumers paying the price.

Compared to the high inflation periods of the 20th century, the post-pandemic inflation surge was modest. If we take seriously claims that the vigor of antitrust enforcement affects inflationary pressures, we should explore why inflation soared in periods of aggressive enforcement in the 20th century. For example, assuming that macroeconomic conditions are irrelevant, one may advance the following speculations:

- The trust-busting campaigns of the early 20th century caused the inflation boom of 1916-1920.

- The rise of antitrust enforcement in the 1930s enabled the inflation spikes of the 1940s.

- The anti-bigness movement of the 1960s caused the Great Inflation (a period of recessions and high inflation).

- The reorientation of antitrust law that began in the late 1970s ended the Great Inflation era and decreased macroeconomic volatility.

- “Techlash,” antitrust populism, and the stacking of the antitrust agencies with crusaders induced the current inflation surge.

The difference between the foregoing baseless hypotheses and antitrust greedflation theories is the attitude toward large corporations. For some, the key explanation for undesirable economic and social conditions is government actions, while, for others, corporate greed is the explanation.

The word “greedflation” is a relatively new political meme, yet theories linking antitrust and inflation theories are far from novel. In his 1952 book, American Capitalism, economist John Kenneth Galbraith noted that, during the post-WWII inflation surge, many believed that rigorous antitrust enforcement could keep prices down and prevent inflation. Galbraith was skeptical of this belief, noting that “the American radical has an unfailing formula” for most economic problems: “demand that the antitrust laws be more rigorously enforced.” Using this unfailing formula, in 1966, Attorney General Nicholas Katzenbach contended that “strong antitrust policy against concentration helps to promote economic growth by making inflation easier to control.” Likewise, in the 1970s, facing an inflation spike stemming from the oil crisis, the Nixon administration blamed the anticompetitive practices of concentrated industries. Thomas Kauper, then the head of the Department of Justice’s Antitrust Division, maintained that strong antitrust enforcement was crucial to the fight against inflation. His counterpart at the FTC, Chair Lewis Engman, emphasized the Commission’s commitment to conduct “an extensive investigation” to ascertain whether the food and oil industries “were limiting competition in an attempt to drive up prices in violation of the antitrust laws.”

Rising Markups in Periods of Disruptions and Inflation

One reason for the parallel rise in profit margins and inflation is the self-fulfilling nature of inflation expectations. Market participants tend to act in ways that align with their inflation expectations. Accordingly, shifts in firms’ inflation expectations tend to affect their pricing strategies. From 2014 to 2020, inflation expectations in the U.S. were relatively stable. However, when inflation started to rise in 2021, inflation expectations also escalated. This pattern partly explains why businesses opted to increase their profit margins.

Several studies confirm or purport to confirm the belief that the rise in corporate profits has indeed contributed to inflation. Some of these studies called to intensify antitrust scrutiny because “[i]ncreasing competition and reducing market power would bring down inflation to some degree, no matter its cause.” In their highly cited paper, The Rise of Market Power and the Macroeconomic Implications, Jan De Loecker, Jan Eeckhout, and Gabriel Unger explain the intuition behind antitrust’s greedflation theories:

Thriving competition between firms is a central tenet of a well-functioning economy. The pressure of competitors and new entrants leads firms to set prices that reflect costs, which is to the benefit of the customer. In the absence of competition, firms gain market power and command high prices. This has implications for welfare and resource allocation. In addition to lowering consumer well-being, market power decreases the demand for labor and dampens investment in capital, it distorts the distribution of economic rents, and it discourages business dynamics and innovation. This has ramifications for policy, from antitrust to monetary policy and income redistribution.

Greedflation theories beg the question of why greedy corporations did not inflate their profit margins before the pandemic. UBS Chief Economist Paul Donovan answered this question, arguing that developed economies experienced profit-margin-led inflation, which he defined as conditions in which “some companies spin a story that convinces customers that price increases are ‘fair,’ when in fact they disguise profit margin expansion.” Donovan observed that companies whose business models rely on customer loyalty ordinarily pass on cost increases, but do not expand profit margins. If consumers feel that prices are rising unfairly, they will abandon the company. However, such companies can use inflation, uncertainty, and external shocks to justify price increases without creating a consumer rebellion. This explanation rests on sound economic principles that address market friction and fairness perception. It has long been understood that companies—small and large ones—can and often do exploit market friction profitably by circumventing fairness perceptions. Be that as it may, antitrust greedflation theories conveniently ignore the global rise in inflation rates. The notion that permissive antitrust policies in the U.S. drove inflation rates around the world seems far-fetched.

Greedflation and Antitrust Thinking

There is a broad consensus among economists and antitrust experts that “competition policy should not be seen as a prominent short-term anti-inflation tool.” The recent flirtation with antitrust greedflation theories aligns with past instances of reckless political maneuvering. It also mirrors the propensity of antitrust populists to propagate misleading, sensational claims. The media’s extensive rejection of these theories suggests that the fervor fueling antitrust populism in recent years has started to wane. The most significant insight that antitrust greedflation theories offer is that political greed sometimes leads to inflated exaggerations, diverting resources toward political memes at the expense of the public.

Articles represent the opinions of their writers, not necessarily those of the University of Chicago, the Booth School of Business, or its faculty.