A stock market that has priced in the transition risk away from greenhouse gasses would see higher future returns, the so-called carbon premium, for carbon-intensive firms that face more risk in a green economy. In new research, Shaojun Zhang finds that the missing carbon premium means that investors are still in the process of pricing in the transition risk as the public navigates the uncertainty associated with climate change in aggregate and at the firm level.

The science broadly agrees that a significant reduction in carbon emissions is required to fight climate change and avoid catastrophe. By December 2021, 236 asset managers had joined the Net Zero Asset Management initiative, which commits signees to support the goal of net-zero greenhouse gas (GHG) emissions by 2050. However, fulfilling this commitment is challenging, because asset managers are bound by their fiduciary duty to singularly maximize the financial aspects of their investments, and calculating the negative impact of climate change on a firm’s bottom line is difficult. In fact, both academics and practitioners heatedly debate if investors materially care about a firm’s exposure to climate change and if markets have priced in the risk.

In my new paper, I study the forward-looking returns associated with a firm’s exposure to the economic transition away from carbon and to green energy sources and infrastructure in the U.S. and internationally in recent years. Intuitively, brown firms (i.e. carbon-intensive firms) are more exposed to carbon-transition risk and thus their investors must earn higher expected returns in equilibrium (when market forces are in balance) in compensation for the risk. This is known as the carbon premium. However, green firms can outperform brown firms when policy shocks kick in, consumer attention turns, and investor tastes shift in transition to the net-zero economy. Alternatively, if investors do not pay attention to firms’ carbon footprints, we would not observe significant outperformance by either green or brown firms.

Measurement and Data

Measuring a firm’s carbon-transition risk is challenging both conceptually and empirically. A few commonly used measures include total carbon emissions, carbon emission growth, and carbon emissions per unit of firm sales (carbon intensity). Carbon intensity is a particularly useful measure of carbon-transition risk in the face of policy shocks, including carbon taxes and cap-and-trade policies, because it recognizes that larger firms are less likely to be affected by the policies compared to firms with the same emissions but lower sales. It also takes into account that carbon-intensive firms are more likely to suffer from shifts in consumer sentiment away from brown products.

Consequently, as many countries implement green policies to reduce GHG emissions and become more carbon-aware, more carbon-intensive firms are theoretically more likely to face declining profitability and stranded assets, have their returns covary more with aggregate carbon policy shocks, and experience lower valuations. Thus, investors in these firms should earn higher expected returns in equilibrium due to the carbon premium.

However, empirical analyses of carbon data do not agree on whether the carbon premium already exists in the data as in equilibrium. Some studies have found the existence of a carbon premium. However, these studies rely on data without sufficient lags in their carbon emissions data. A firm’s total emissions grow in proportion to and contain information about firm production. Sufficient data lags are necessary to make sure the data is available to investors before correlating them to returns. Without this lag, analyses can generate inaccurate returns reliant on future profitability news rather than actual carbon risk. The firm carbon emissions data in my study has a median lag of ten months. Typical accounting information usually only observes a six-month lag.

Carbon Returns in the US and Internationally

A firm’s carbon emissions fall into three categories or scopes. Scope 1 GHG emissions cover direct emissions from a firm’s owned or controlled sources. Scope 2 GHG emissions cover indirect emissions from the generation of purchased electricity, steam, heating, and cooling consumed by the reporting company. Scope 3 GHG emissions include all other indirect emissions that occur in a company’s value chain. Due to data limitations, I mostly focus on the upstream scope 3 emissions.

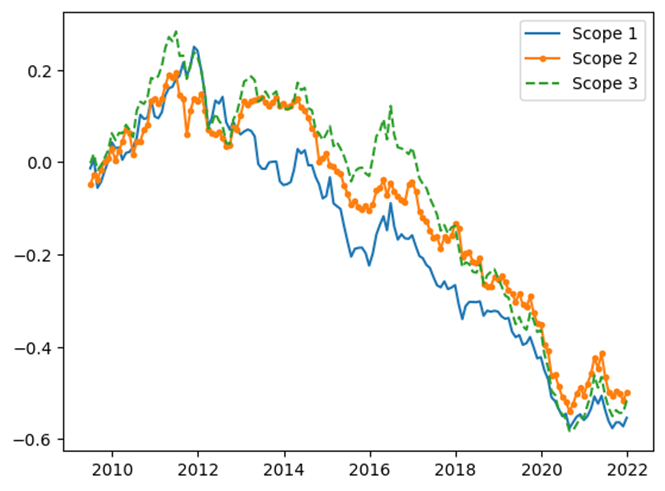

In the U.S., brown firms have earned lower future returns than green firms in recent years. Figure 1 shows that a trading strategy that longs more carbon-intensive firms and shorts fewer carbon-intensive ones loses more than half of its initial value over the sample period. The outperformance of green firms relative to brown firms cannot be explained by risk factors driven by broad market movements, such as the market return, performance of value stocks, etc. Moreover, the return spread sources only from green industries outperforming brown ones and green firms do not outperform the brown ones within an industry.

Figure 1: U.S. Cumulative Excess Carbon Return

The analysis also reveals that there is no carbon premium or excess return associated with total emissions or total emission growth in the U.S., suggesting that these measures do not capture the carbon-transition risk. In short, the evidence strongly suggests that the carbon transition is underway in the U.S., but investors have yet to price in firm-level carbon risk. In other words, there is no real carbon premium for U.S.-listed firms.

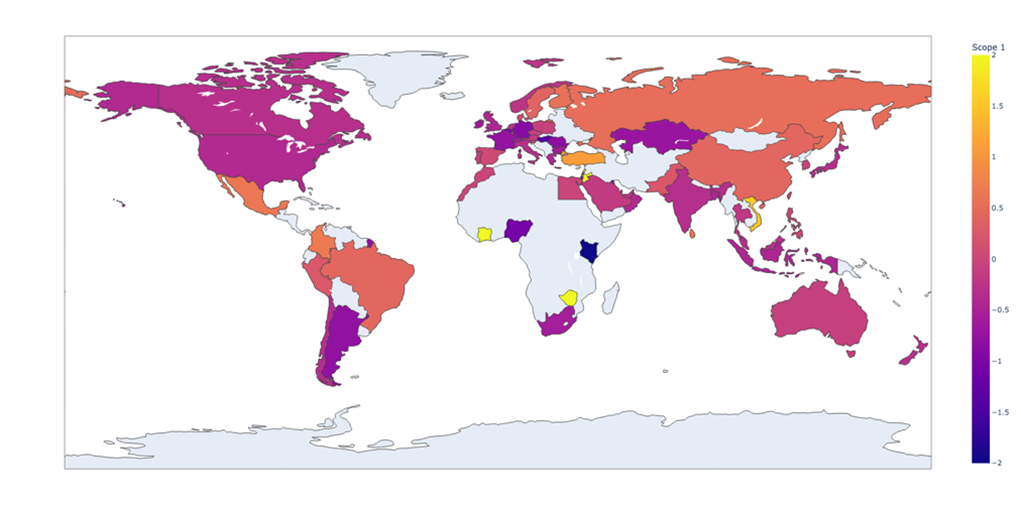

Internationally, there is no robust outperformance by the brown or green firms on average at first glance. However, global carbon returns show a huge dispersion across countries. One possible interpretation is that investors worldwide do not really care about the carbon risk and the fact that green industries have recently outperformed brown industries in the U.S. as documented above is merely a result of data mining. Alternatively, shifts in investors’ preferences have differed widely across countries during the global green transition, generating a mean carbon-risk return close to zero but with significant variance across countries that obscures the carbon premium.

Indeed, Figure 2 indicates lower risk-adjusted carbon returns in more developed countries on average. Two possible interpretations follow. First, investors in more developed countries care about climate change less and price in less carbon risk in equilibrium. Alternatively, the developed markets, including the U.S., are transitioning to the new net-zero equilibrium faster, generating lower carbon returns due to shocks in taste and policy.

Figure 2: Country-Level Abnormal Mean Carbon Returns

I measure the shift in investor preference by country-level sustainable flows and surveyed climate concern. Developed countries have experienced stronger climate-aware shifts in both investor and consumer preference, generating lower carbon returns. This evidence strongly suggests that the transition to the new equilibrium with full carbon awareness is aggressively underway in developed countries. Carbon returns for brown firms remain subdued as investors adapt to the green transition, though in time the expected carbon premium will likely become clearer.

In addition, after controlling for in-sample shocks, I find that firms operating in countries with a higher physical exposure to climate change earn higher carbon returns in sample, suggesting that investors are considering carbon risk due to climate exposure at the national level. However, no other country-level characteristics, such as carbon dependency and institutional governance, impact current levels of carbon returns.

Conclusion

The carbon transition is aggressively underway in the U.S. and global stock markets. As a result, carbon returns can fluctuate significantly. Future returns depend not only on the expected carbon premium in equilibrium but also vary with future shifts of public attention to climate change, investor preference, and climate policy. It is therefore crucial to communicate to investors the properties of green returns during the transition and to caution against forming expectations about future carbon returns based on past performance.

In light of the challenges to determining future short and long-term returns on carbon exposure, the two largest asset managers have withdrawn from actively screening the firm-level carbon risk, recognizing their role in the transition as a “fiduciary” to investors (see statements by Blackrock and Vanguard). While the withdrawals may seem like a blow to ESG investing and net-zero ambitions, it is important to recognize that encouraging investors to chase excess returns by green firms in the short run not only hurts the investors’ financial wealth but also hurts investors’ support for carbon reduction and net zero in the long run. Combating climate change has a long way to go and thus only sustainable long-term investing can help achieve the goal.

As a final comment, investors recognize that total emissions or emission growth do not capture carbon risk and extremely harsh green policies that limit each firm to a fixed quota of carbon emissions do not impose material transition risks on firms. This may be because companies can circumvent these policies by spinning off pollutant plants and brown subsidiaries. If this is the case, the future economy would be less concentrated but with no effective material carbon reduction. Instead of aggressive green policies targeting total emissions, shifts in consumer sentiment and softer policies, such as the carbon tax and cap-and-trade, will likely prove to be more effective in combating climate change and achieving a net-zero economy.

Disclosure: Zhang received financial support for her research from the Hong Kong Institute for Monetary and Financial Research. Read about our disclosure policy here.