A 2000 amendment to the Hart-Scott-Rodino Act made it easier for firms to merge without notifying US antitrust authorities. In new research, Giovanni Morzenti writes that while deregulation has facilitated some mergers that boosted innovation, on the whole it has enabled inefficient mergers to the detriment of consumer welfare and market innovation.

Merger activity is rising, and 2021 saw a record-setting year in global M&A activity. The economic literature produces mixed predictions on how mergers and acquisitions shape the returns and the incentives to innovation. On the one hand, mergers can encourage firms to innovate more, as less competition allows them to capture a higher share of innovation returns. On the other hand, less competition means that firms have fewer incentives to innovate to defend their market positions. In new research on how a relaxation of pre-merger notification rules corresponded to changes in patent activity, I find that mergers no longer deterred by antitrust authorities lead to lower innovation overall. This effect is particularly pronounced among horizontal mergers, i.e. mergers between firms that occupy the same product market. Non-horizontal mergers that take advantage of synergies are more likely to boost innovation.

Deterred mergers are those that the firms do not even attempt because they know that antitrust authorities will block them. However, not all mergers are subject to antitrust scrutiny. In the US, like in many other countries, a pre-merger notification to the authorities is required only for larger mergers. As such, only mergers that need to notify the antitrust authorities can be deterred.

In December 2000, the US Congress passed an amendment to the Hart-Scott-Rodino Antitrust Improvements Act that made these pre-merger notification requirements significantly more lenient by raising the threshold at which firms are required to notify a merger. The amendment raised the threshold for antitrust’s “size of person” test, i.e. the asset value of the target firm in the merger, from $10 million to $50 million. Any merger in which the target firm had less than $50 million in assets no longer required pre-notification.

However, more impactful on subsequent reporting was the amendment’s introduction of a second test, known as the “size of transaction” test. This new test exempted from pre-notification any merger in which the transactional value was less than $50 million.

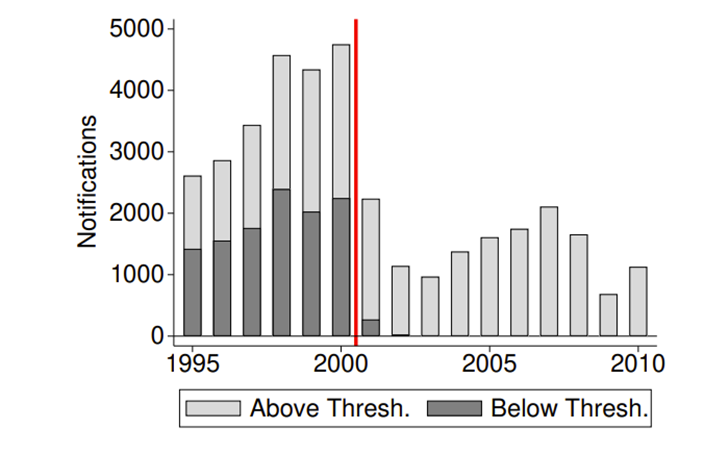

This policy change, one of many instances of US antitrust deregulation over the past decades, was so impactful that the number of pre-merger notifications received by the US authorities decreased by 70% from 2000 to 2002. Congress did not appear to anticipate the magnitude of this policy change: it was passed as four pages buried within a 320-page omnibus bill approved at the end of the Clinton administration.

Figure 5: Number of Notifications received by US Antitrust Authorities

If a merger is notified, the authorities can issue a second request asking for more internal documents if they have concerns regarding the transaction. The number of second requests issued by the Federal Trade Commission and the Department of Justice decreased by 50% from 2000 to 2002. Not only did the US government oversee fewer mergers, but among those firms still required to notify the US government, the share of notifications resulting in second requests decreases from 5% to 3%.

The change in antitrust regulation in 2000 allows researchers to compare the activity of mergers that before the change would have had to notify the government but no longer needed to with those mergers that did notify the US government before the amendment. Research from Thomas Wollman shows that the 2000 amendment generated about 300 horizontal mergers per year that were not notified to the authorities.

These unreported horizontal mergers, or so-called stealth consolidations, are the ones that the authorities would have likely deterred. Therefore, they inform us on the potential deterrence effect of merger policy on innovation. Since the policy change, non-notified horizontal mergers have led to 30% less innovation compared to mergers that are still notified, based on subsequent patent activity. Some of these mergers might be beneficial to innovation, but the overall effect was negative, on average. For mergers that would have been deterred by the authorities in the absence of the 2000 amendment, lower incentives to innovate due to market power tend to prevail over the stronger appropriability of innovation returns.

These findings are not dependent on the definition of horizontal mergers or even on the measure of innovation activity. Pharma and Big Tech are the sectors where the effect of the amendment is strongest. However, these sectors tell two different stories due to the role of horizontal mergers. In Pharma, horizontal mergers tend to be detrimental to innovation, while non-horizontal mergers have little-to-no effect. Thus, deregulation inhibited innovation in the sector. In Big Tech, where horizontal mergers are less common, the amendment had less notable impact. Instead, the sector continued to take advantage of synergies via non-horizontal mergers, which are on average more beneficial to innovation. This discrepancy between Pharma and Big Tech reveals that not all mergers harm innovation or should be deterred.

The extent of synergies between merging firms, the presence of economies of scale, the possible removal of redundancies, the spreading of innovation on more assets, these are all called efficiencies in the merger literature. The higher the efficiencies, the better the merger outcomes, both in terms of innovation and consumer welfare. Two firms merge because they expect higher profits, and these can come from efficiencies or from market power. The merging firms must prove the existence of significant efficiencies to the authorities so as to counterbalance the possible anticompetitive effects of their proposed merger. Mergers generating little or no efficiencies are detrimental to innovation and to consumer welfare, and these are the ones that should be deterred by merger enforcement.

The data corroborate this interpretation, as horizontal mergers that are not notified to the authorities reduce innovation, compared to notified horizontal and non-horizontal mergers. Given their negative effect on innovation, we can infer non-notified horizontal mergers generate few efficiencies. Consequently, these transactions are also detrimental to consumer welfare.

The relaxation of merger enforcement has had unintended consequences. Lax merger policy can spur a merger wave, enabling the worst transactions in terms of innovation and consumer welfare. Although the 2000 amendment to the Hart-Scott-Rodino Act concerned large mergers, policymakers should not dismiss small mergers as negligible for competition and innovation. Indeed, the FTC cited these very concerns when it issued special orders compelling Big Tech to disclose previously non-reportable deals. Similarly, The New York State Senate passed a bill creating a first-of-its-kind state-specific pre-merger notification rule, specifically aimed at the Big Tech sector.

Several other countries followed the US and likewise relaxed their pre-merger notification rules. Many of these countries similarly show evidence of stealth consolidation. Undoubtedly, deliberate antitrust deregulation has contributed to the unwavering merger activity that characterizes the contemporary global economy. The concentration of asset ownership via mergers can also explain part of the rise in market power that has been documented in the US and on a global scale. Rising market power redistributes resources toward firm owners, accentuating existing inequalities. Deregulation can facilitate market synergies, but too often deregulation has empowered M&A activity that achieves little efficiency and only increases firms’ profits at the expense of consumer welfare and innovation. Policymakers must return to a robust, if nuanced, antitrust policy to limit market power, benefit consumers, and encourage innovation.